INVESTMENT RETURN METRICS AND EQUITY STRUCTURES

I often hear questions about return metrics and equity structures for real estate investments. Return metrics assess an investment’s profitability, while equity structures provide a framework for distributing net cash flow, returning capital, and allocating profits to investors. There isn’t one universal way to structure equity in an investment. The specific needs and circumstances of the opportunity determine the most effective approach.

Here is a quick summary of key terms and definitions to consider when investing in real estate.

Cash-on-Cash Return/Yield

This metric measures the annual return on an investment based on the cash flow generated by a property relative to the total equity invested. It is calculated by dividing the annual pre-tax cash flow after debt service by the total equity investment.

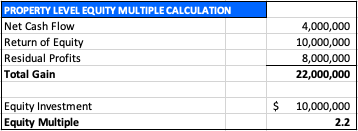

Equity Multiple or Multiple on Invested Capital (MOIC)

This multiple is a financial metric that measures the total return (in dollars) of an investment relative to the initial equity invested. It is calculated by adding the total cash flow during the holding period, the return on equity, and the return of equity, and then dividing this sum by the equity investment.

Internal Rate of Return (IRR)

The IRR measures an investment’s profitability over time and is expressed as a percentage. This metric includes cash flow during the holding period, the return of equity, and the return on equity. It inherently incorporates the time value of money concept—another way of saying that a dollar today is worth more than a dollar tomorrow. The IRR helps investors compare different investment opportunities and determine which offers the most attractive risk-adjusted return.

Preferred Return

This return is a predetermined profit distribution where investors receive a specified return on their equity investment. It is a predetermined hurdle rate or minimum return that must be met before the sponsor earns the “promote” or “carried interest.”

Promote or Carried Interest

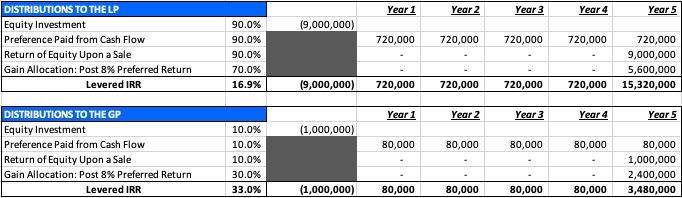

The “promote” is an incentive for the general partner (GP) to receive a disproportionate share of the profits relative to their equity contribution once they achieve the preferred return. For example, a 90/10 structure refers to a joint venture arrangement in which the limited partner (LP) contributes 90% of the project’s equity, and the GP invests 10%. The preferred return is 8%, and distributions are split based on the initial investment percentages up to this hurdle rate. Once the preferred return is met, distributions beyond this return are split 70% to the LP and 30% to the GP. This split can also be referred to as a “waterfall distribution.”

Equity structures come in all shapes and sizes, meaning there are many different ways to structure equity investments. It largely depends on the risk involved with the opportunity and whether it is a core, value-add, or opportunistic investment.

What is more important, an IRR or equity multiple? The answer is entirely investor-specific. An IRR may be more important for investors measuring the return over a short-term holding period. However, the equity multiple may be an ideal metric for investors seeking a higher return on their initial investment over a longer holding period. BAM Capital has provided and offers an optimal blend of both.

Disclaimer: This document is for informational purposes only and is not financial, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by Bam Capital are made pursuant to Rule 506(c) of Regulation D and are available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC). Verification of accredited investor status is required before participation in any investment. The information contained herein reflects the opinions of the author and does not necessarily represent the views of Bam Capital. Any financial terms, projections, or forward-looking statements contained herein are hypothetical in nature and should not be interpreted as guarantees of future performance or safety. Such statements reflect opinions and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including but not limited to illiquidity, economic downturns, and potential loss of invested funds. Past performance does not guarantee future results. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions. Bam Capital makes no representation or warranty regarding the accuracy or completeness of the information contained herein.

© 2025 Bam Capital. All rights reserved.

Author: Tony Landa, Senior Economic Advisor, The BAM Companies, July 2025