Disclaimer: This content may contain forward-looking statements based on current economic conditions and third-party data sources. Actual results could differ materially due to shifts in market conditions, policy decisions, or other macroeconomic variables.

After a turbulent two-year stretch marked by rising interest rates and aggressive new construction, 2025 emerged as a year of cautious recalibration for the multifamily investment sector. National multifamily investment returns have begun to stabilize as borrowing costs edge lower and rent growth returns to positive territory. Recent data suggests moderate but meaningful improvements.

Average Multifamily Investment Returns, 2025 | |||

Strategy Type | Target Net IRR | Risk Profile | Best For |

Core / Core-Plus | 6-10%/ 8-12% | Low–Moderate | Investors prioritizing income stability and predictable returns |

Value-Add | 11-16% | Moderate | Investors seeking higher total returns through property improvements |

Opportunistic / Development | 16%+ | High | Investors comfortable with higher risk and longer timelines for outsized growth |

2025 Multifamily Investment Returns by Strategy and Region

Multifamily Investment Returns by Strategy

By mid-2025, performance across investment strategies showed greater consistency.

Investment Strategy | Typical 2025 Internal Rate of Return | Cash-on-Cash Range | Market Dynamics |

Core / Core-Plus | 6-10%/ 8-12% | 5–7% | Stable income assets benefited from lower cap rates and renewed refinancing activities as lending conditions slowly improved. Returns stayed moderate but reliable, appealing to investors focused on steady income. |

Value-Add | 11-16% | 6–9% | Execution improved as renovation backlogs cleared and rents recovered. Midwest and secondary markets performed relatively better. |

Opportunistic | 16%+ | Variable | Selective success, with strong outcomes in rebounding urban submarkets but high risk tied to refinance exposure. |

While headline numbers may not match pre-2023 levels, the return environment appears to be normalizing. Investors are once again pricing assets based on long-term income potential rather than short-term speculation.

Outlook for 2026:

- If current trends continue, the internal rate of return (IRR) ranges could modestly improve as interest rates ease, construction slows, and rent growth stabilizes.

- Value-Add and Core-Plus strategies may offer some of the most balanced risk-adjusted opportunities, particularly in supply-constrained Midwest markets.

- Opportunistic deals could see wider variation in outcomes depending on timing and local recovery strength.

Multifamily Investment Returns by Region

Geographic diversification remains one of the defining advantages of multifamily investing. Yet, performance across U.S. regions in 2025 reveals how structural fundamentals can drive regional outperformance.

Region | 2025 Avg. Rent Growth | Vacancy Rate | Typical Value-Add IRR | Outlook for 2026 |

Southeast | -2% to +3% | 6% to 11% | 12–16% | Demand remains solid across the Southeast, but heavy deliveries in markets like Nashville, Tampa, and Atlanta continue to pressure rent growth and elevate vacancy. The region still offers strong long-term upside, though with greater short-term volatility. It’s best suited for investors comfortable with more cyclical performance. |

Midwest | 1.5% to 4.5% | 4% to 8% | 11–15% | Moderate, steady growth remains the defining feature of the Midwest. Across major Midwest metros, rent growth has held in the low- to mid-single digits while vacancy sits in the mid-single digits, even with new deliveries. The region remains attractive for investors seeking durable income, lower volatility, and more predictable cash flows rather than aggressive, cycle-driven upside. |

Coastal Metros | 0% to 3% | 3% to 7% | 9–13% | Growth may stay constrained by regulation and affordability limits. However, well-located Class A and “necessity housing” assets could see renewed investor interest if financing conditions continue to ease and new construction remains muted. |

Sun Belt | -4% to +2% | 7% to 12% | 12-17% | Conditions appear to be stabilizing after several years of heavy deliveries. While many Sun Belt metros still face elevated vacancy and rent softness through mid-2026, absorption is strengthening as new construction finally tapers. Long-term tailwinds remain intact, but near-term performance is likely to stay uneven and more cyclical than other regions. |

Midwest markets remain the most consistent performers, with rent growth in the 1.5%–4.5% range, vacancy around 4%–8%, and typical value-add returns of 11%–15%.

The Southeast and Sun Belt continue to draw long-term demand but face short-term pressure from elevated supply and softer rent growth. Coastal metros show modest recovery, with low single-digit rent gains and mid-single-digit vacancy constrained by regulation and affordability.

As 2026 approaches, the Midwest’s combination of affordability, job diversity, and supply discipline positions it as one of the most stable regions for predictable cash flow.

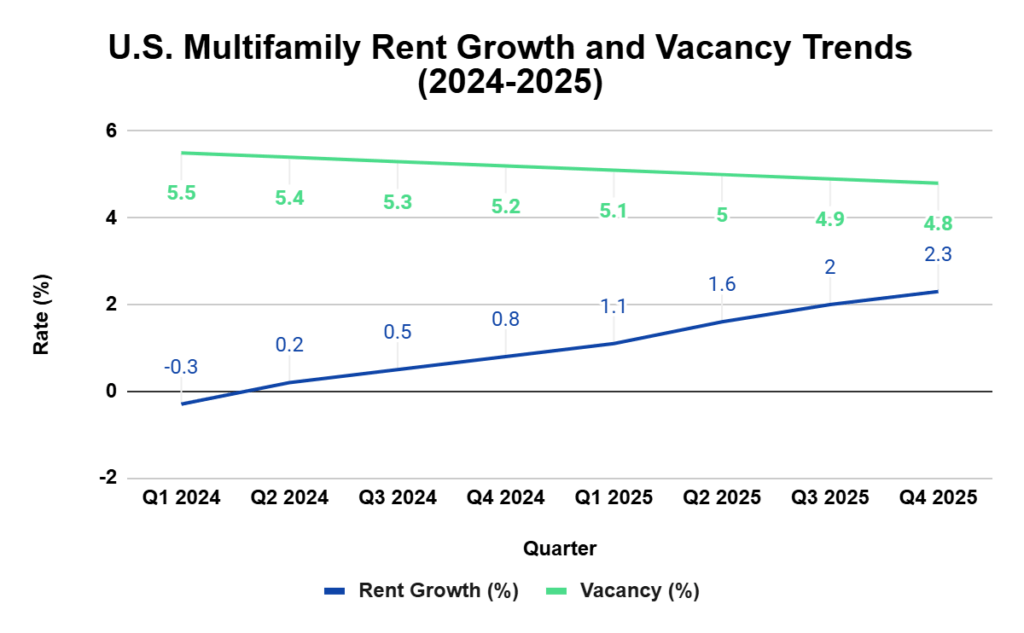

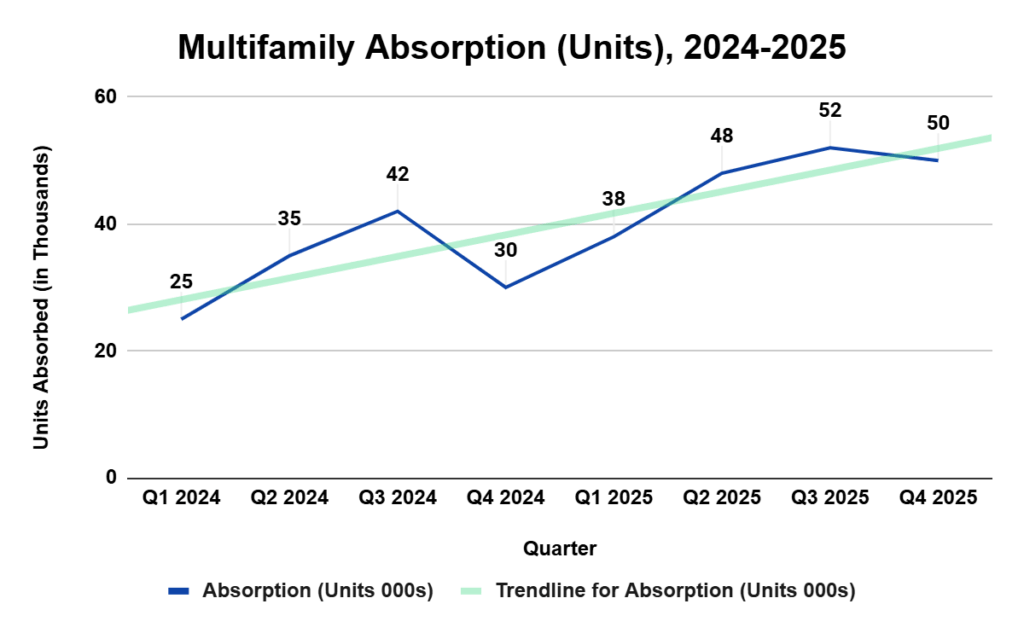

2025 Marked a Transition Toward Stability

These graphs show that multifamily fundamentals began stabilizing through 2025. Rent growth, which had flattened in early 2024, gradually turned positive as vacancies declined below 5%. At the same time, absorption rebounded—particularly in affordable regions—signaling renewed renter demand and steady leasing momentum. For investors, this combination of rising occupancy and modest rent growth points to a market entering a healthier, more sustainable phase rather than another boom-and-bust cycle.

Key performance themes in 2025:

- Demand recovery: Leasing velocity strengthened through Q2 and Q3 2025, especially in Midwest and Sun Belt metros, as household formation rebounded. Renewal rates climbed above 60%, with renters opting to extend their leases as affordability improved and rental markets normalized.

- Rent normalization: Concessions that were common in late 2024 were largely phased out by mid-2025. Effective rents rose 1.5–2.3% year-to-date, while NOI (Net Operating Income) growth turned positive again by Q3 as operating efficiencies improved.

- Capital market thaw: Transaction volume rose ~25% year-over-year as credit spreads narrowed and lenders re-entered the market. Sponsors with strong balance sheets secured refinancing at materially lower costs than in 2024.

- Supply reset: New construction starts fell nearly 40% across several metros, easing short-term competition. Absorption outpaced deliveries by late 2025, helping stabilize vacancy levels around 4.8%.

These shifts hint at a sector that may be regaining balance after years of rapid expansion and contraction.

Interest Rate and Cap Rate Dynamics

Interest rates continue to shape multifamily investment returns in 2025. After two years of sustained tightening, the Federal Reserve’s late-2024 pause and gradual moderation may have created a more favorable financing environment throughout the year.

- The 10-year Treasury yield declined roughly 60 basis points from Q1 to Q4.

- Cap-rate spreads compressed toward 2019 levels, improving underwriting confidence and buyer-seller alignment.

- Transaction volume potentially increased as financing costs stabilized and lending terms normalized.

This neutral-to-positive rate environment has supported greater valuation stability without re-inflating prices.

2026 outlook: Looking ahead to 2026, modest additional rate relief could further strengthen transaction momentum, especially for stabilized and value-add properties using conservative leverage.

Key Risk Factors for Multifamily Investors in 2025 and Beyond

While fundamentals improved through 2025, several structural and market variables continue to impact return potential and overall risk exposure:

- Refinancing Pressure: Roughly $89.3 billion in multifamily loans come due in 2026, and refinancing could become a challenge if lending spreads stay wide. Sponsors with moderate leverage and fixed-rate financing are likely to be better positioned than those carrying floating debt or higher loan-to-value ratios.

- Insurance and Property Taxes: Nationally, per-unit insurance expenses increased nearly 28% year-over-year and roughly 75% since 2019. Some owners—particularly in coastal and Sun Belt markets facing higher climate risk—reported premium jumps ranging from 15% to over 40%. In more stable Midwest metros, increases have generally been more moderate, helping preserve NOI margins despite broader operating-cost inflation.

- Residual Oversupply: Several Sun Belt metros continue to work through elevated delivery pipelines, which is weighing on rent growth and occupancy. Austin, for example, recorded the highest concessions rate in the U.S. at 30.5% in August 2025, reflecting ongoing supply pressure . Analysts also note lingering oversupply in Phoenix, Atlanta, and other fast-growth Sun Belt markets tied to aggressive pandemic-era construction. Midwest metros, with smaller pipelines and steadier absorption, remain more balanced.

- Policy and Regulation: Localized rent control measures in high-demand states like California and Minnesota could introduce compliance challenges, while property tax reassessments in growth markets may tighten cash flow.

Overall, the risk outlook appears manageable for investors and sponsors, emphasizing conservative leverage, disciplined underwriting, and operational efficiency. The focus, as always, is on selecting markets and managers with the ability to adapt to shifting conditions.

Investment Timing: Why Late 2025 May Offer an Opportunity

For investors with a long-term outlook, late 2025 may represent an attractive entry point, one that allows capital to capture improving fundamentals without chasing peak pricing.

- Favorable Basis Pricing: Acquisitions made in 2025 could benefit from recalibrated pricing that reflects normalized rent assumptions and moderate cap rates. Many owners who financed during the 2021–2022 peak cycle are choosing to sell rather than refinance at higher rates. This shift is creating a rare opportunity to acquire well-located, income-producing properties, potentially at healthier valuations, without competing in inflated conditions.

- Improving NOI Growth: As rent concessions phase out and expense growth moderates, NOI recovery is likely to accelerate. Analysts project NOI growth of 3–4% annually through 2026 as occupancy stabilizes and operational efficiency improves.

- Lower Delivery Pipeline: The multifamily construction pipeline is showing signs of volatility, not a clean slowdown. While starts have dipped in some recent months (likely due to higher borrowing and construction costs), completions remain elevated, and 2025 has already seen sporadic rebounds in starts. The mixed signals suggest that supply risk persists, but the development pause many expected has not fully materialized. This environment sets up a bifurcated market: stabilized assets and markets with modest supply growth may see healthy absorption, while metros with high concentrations of new deliveries could still face downward rent pressure.

- Potential Rate Easing: The Federal Reserve’s gradual policy normalization could continue to lower borrowing costs through 2026. Even modest rate reductions may expand investor purchasing power and improve refinance economics for sponsors with conservative leverage.

- Portfolio Positioning: Leading sponsors are concentrating on stabilized and light value-add assets with strong in-place cash flow and manageable refinancing exposure. It’s a measured approach that may help create a more predictable return environment as the market transitions into a steadier rate cycle.

While conditions differ market to market, the 2026 forecast points to steady progress in core fundamentals. Rent growth could edge toward 3–4% nationally as new supply slows and borrowing costs continue to ease. Vacancy rates may hover near 4.5–4.8%, suggesting a more balanced environment for income and value appreciation.

For investors focused on stable, income-producing assets with moderate leverage, this period may represent one of the strongest vintages of the current cycle, offering a combination of disciplined entry pricing, improving fundamentals, and long-term growth potential.

How Leading Sponsors Are Preparing for 2026

Sponsors with disciplined, vertically integrated operations appear best positioned for the next phase of the multifamily cycle. After two years of capital market volatility, execution and efficiency are again defining success.

BAM Capital’s investment philosophy, for instance, continues to emphasize long-term durability through:

- Regional Discipline: BAM Capital focuses on resilient Midwest metros such as Indianapolis and Kansas City: markets that continue to post healthy rent-to-income ratios. Even as broader markets softened, these cities maintained strong absorption and stable renter demand, thanks to diverse employment bases and steady population growth.

- Operational Integration: Every stage of BAM Capital’s process, acquisition, construction, and property management, is managed in-house. This structure gives the firm tighter control over costs, timelines, and the resident experience.

- Conservative Leverage: Debt discipline remains central to BAM Capital’s strategy. Through balanced debt levels maintenance, the firm preserves flexibility during refinancing cycles and protects investors from unnecessary rate volatility.

- Performance Consistency: BAM Capital’s historical approach, emphasizing preferred distributions, transparent reporting, and proactive communication, has earned the confidence of its investors.

This shift marks a move from growth at all costs to performance built on discipline and data traits that may ultimately define the sponsors best positioned heading into next year.

Steady Returns, Selective Upside

Multifamily investment returns in 2025 tell a story of normalization, not exuberance. The market appears to be rebalancing after several volatile years, with stable income and modest appreciation taking precedence over aggressive growth.

While national returns may average in the low-to-mid teens on a gross levered basis, regional and sponsor-level variations could be wide. For accredited investors seeking risk-adjusted performance, the Midwest continues to stand out as a practical, income-focused market where fundamentals drive returns.

Ready to see if we’re the right fit for your portfolio? Schedule a call today to learn how BAM Capital can help you build long-term wealth through our real estate syndication returns.

Disclaimer: This article is for informational purposes only and is not financial, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by Bam Capital are made pursuant to Rule 506(c) of Regulation D and are available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers. Verification of accredited investor status is required before participation in any investment.

Any financial terms, projections, or forward-looking statements contained herein are hypothetical in nature and should not be interpreted as guarantees of future performance or safety. Such statements are based on current expectations, estimates, and assumptions, which are inherently subject to uncertainties and contingencies, many of which are beyond Bam Capital’s control. Such statements reflect Bam Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Actual results could differ materially from those projected or implied in any forward-looking statements.

Investing in private real estate securities involves significant risks, including but not limited to illiquidity, economic downturns, and potential loss of invested funds. Past performance does not guarantee future results. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2025 Bam Capital. All rights reserved.

For additional multifamily real estate insights, visit Pathways to Passive Wealth, BAM Capital’s new platform designed to make real estate investing more accessible, transparent, and achievable for aspiring and experienced investors.