Real estate syndication or private placement is an investment in which multiple investors pool their capital to purchase a single property or portfolio. A sponsor, also known as a syndicator, handles everything from locating the investment property to assembling the deal, securing financing, negotiating with the seller, conducting due diligence, collecting rental income, and distributing the cash flow among the investors. [1] As active investors in multifamily private placements, a general partner (GP) or sponsor plays a crucial role in managing the investment from acquisition to sale, including property management, decision-making, and reporting to investors. Meanwhile, limited partners (LPs) are passive investors. [2][3]

Owners can accomplish syndication with almost any type of real estate property, but when done with a multifamily property, it is referred to as multifamily syndication or private placement. Multifamily syndication is attractive because it is a potentially lower-risk investment.

Multifamily properties, such as apartment communities, often feature numerous units that can generate substantial cash flow. Additionally, they are not heavily impacted by vacancies, unlike single-family real estate properties. For example, if a property has 50 units with 45 occupied, the property is still in a stable position. Meanwhile, with single-family residences, your income goes to zero if the resident leaves.

Depending on the deal structure, passive investors provide a portion of the capital required in exchange for monthly or quarterly income distributions from the asset or a share of the equity upon resale. [3]

Trustworthy syndicators have diverse expertise and a more well-rounded team, providing increased investment potential. They possess a deep understanding of due diligence for potential deals, enabling them to handle every step of the syndication process, thereby making it a true passive investment for limited partners (LPs). [2]

How Does Multifamily Syndication Work?

Structure of the Deal

General Partners (GP) | Sponsor | Syndicator

Role

- Puts together the private placement offering.

- Identifies an investment property, secures financing, and partners with passive investors, known as limited partners (LPs).

- Oversees daily operations directly or via a third party.

- Executes the business plan.

- Manages construction or renovation projects.

- Monitors financial performance.

- Ensures compliance with lender requirements and government regulations.

- Sends regular investor updates and reporting.

- Manages distributions and tax documents.

- Prepares the property for exit. [4]

Tasks

- Deal sourcing

- Securing loans

- Negotiating purchase terms

- Conducting due diligence

- Managing renovations

- Maintaining investor relations

Limited Partners (LP) | Passive Investor

Role

- Provides a portion of the capital and earns money from the cash flow and/or the equity, depending on the deal structure.

- No active management responsibilities.

- Experiences the benefits of real estate investment, such as income generation, tax benefits, diversification, and property appreciation, all without the operational complexities of managing a property.

Syndication Fees & Structure

This fee compensates the general partner for the time required to identify and perform due diligence on an acquisition. They take charge of the whole thing from start to finish. [5] The acquisition fee can be 1% to 5% of the purchase price. The fee can be above 5% or less than 1%, but these are much less common. For example, if a sponsor’s acquisition fee was 2%, and the real estate property was $1 million, the sponsor would be paid a one-time acquisition fee of $20,000. [5]

Developers typically handle construction in a multifamily investment deal. They will partner with a sponsor and its investors who provide equity. Sponsors can then charge a fee for managing the relationship with the developer, ranging from 2% to 8% of the total development or construction cost. [5]

The asset management fee is another way general partners earn from multifamily private placement deals, and it is paid to oversee the property’s operations and manage the business plan. It can be collected in two ways: it may be charged as a percentage of income; in this case, the standard is 2%, or it can be collected as a cost per apartment unit per year. [5]

The disposition fee, sometimes called an “exit” fee, is paid to a sponsor for marketing efforts and facilitating the property sale. It typically ranges from 0.5% to 2% of the sale price. Since the disposition fee is usually tied to the property’s performance, it is in a sponsor’s best interest to obtain a competitive offer and deliver the highest possible returns to its investors. [5]

Equity raise fees, also known as fundraising fees, represent a percentage of the total equity raised in a deal (typically 1% to 3%) paid to a sponsor for their success in raising capital, driving sales, and securing investors. This fee is usually paid at the close of a sale, after equity has been raised, to compensate sponsors for the resources they have invested in sourcing capital for the deal. [5] Note that the fees mentioned above are not immutable and are subject to the deal structure and the sponsor’s discretion. They vary based on the sponsor, the deal’s complexity, and the market. A well-structured fee model should strike a balance between providing fair compensation to the sponsor and considering the returns of investors. [5]

Multifamily Financing Options

Banks

Bank loans are traditional financing options used for multifamily properties. They are among the most common loans that banks and other financial institutions offer. [6] These loans are issued and held by banks or credit unions rather than being sold on the secondary market like agency or CMBS loans. Borrowers who opt for a conventional bank loan often intend to purchase or refinance a property. Bank loans can be offered at a fixed or floating interest rate, frequently requiring a substantial down payment, a positive track record, and a good credit profile. [6] Bank loans are ideal for borrowers with unique needs, as terms can be tailored to work in their favor. Interest rates can be higher with bank loans than agency loans, and loan terms may be shorter or include more frequent requalification requirements. [6]

Commercial Mortgage Backed Security

CMBS stands for “commercial mortgage-backed securities.” A commercial mortgage-backed security is a fixed-income investment instrument backed by mortgages on commercial properties. Like agency loans, CMBS loans can provide non-recourse financing for commercial multifamily properties valued at $2 million or more, with loan-to-value (LTV) ratios of up to 75%. CMBS loans are fixed-rate and can be less flexible than other types of loans. However, they offer potentially less scrutiny for borrowers who do not meet agency requirements. The trade-off for less scrutiny is generally stricter prepayment penalties and standardized (i.e., inflexible) terms that cannot be easily changed after loan origination. Once issued, CMBS loans are securitized, sold, and traded in a pool of other CMBS loans on the secondary market.

Agency Loans

Agency loans are typically more nuanced than conventional bank loans because they are backed by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac. GSEs generally offer 5- to 10-year fixed-rate balloon loans. In other words, borrowers make a series of fixed-rate payments where the interest rate remains constant for the duration of the loan. At the end of the loan term, the borrower makes a final, large payment, known as a balloon payment, to settle the remaining balance. Agency loans are also generally nonrecourse loans. Freddie Mac and Fannie Mae tend to have lower interest rates than other loan types, but they include more stringent terms, such as prepayment penalties, higher borrower qualification standards, and loan-to-value (LTV) limits. These terms aim to ensure that borrowers are qualified (capable of repayment) and avoid fraudulent behavior. Because of these requirements, agency loans are typically best suited for stabilized properties (a property that has reached favorable occupancy, income, and expense levels). [6]

Housing and Urban Development (HUD)

HUD loans are mortgages insured by the U.S. Department of Housing and Urban Development (HUD). HUD loans are popular for commercial real estate and multifamily properties because they offer favorable financing terms, such as lower down payments and more lenient credit score requirements. HUD loans can have potentially lengthy loan terms (40 years or more) and are fixed-rate, fully amortizing loans for the entire loan term. One of the most well-known HUD programs is the HUD 221 (d)(4) loan. This program is designed to finance renovation and ground-up development projects. While many construction loans are short-term and interest-only, HUD 221 (d)(4) loans are unique because they combine construction and permanent financing into one long-term loan, offering up to 43 years of fixed-rate, fully amortizing repayment. [6]

How Much Money Do Syndication Investors Make?

IRR

The internal rate of return (IRR) is a critical metric in multifamily real estate that measures the lifetime profitability of an investment product and is expressed as a percentage. IRR is the discount rate that makes a project’s net present value (NPV) zero. It includes cash flow during the holding period and is calculated to determine the potential rate of return. The exact IRR formula is complex and is often calculated using financial software or Excel. In other words, it is your return on equity, with a time value of money (TVM) component. So, a dollar today is worth more than five years from now. [7]

Importance:

- Comparative Tool: It allows investors to compare different investment opportunities fairly, regardless of size or duration. [8]

- Performance Measure: Reflects the efficiency of an investment, taking the time value of money into account.

- Decision-Making: Helps investors assess whether a property meets their required return threshold, taking into account risk and opportunity cost.

Limitations:

- Reinvestment Assumption: Assumes cash flows are reinvested at the IRR, which may not always be practical.

- Complementary Metrics: For a well-rounded analysis, complementary metrics should be used with other indicators like cash-on-cash return and equity multiple.

IRR is crucial for assessing potential real estate investment returns, but it should be used in conjunction with other financial metrics.

Cash-On-Cash Return

This metric is a rate of return that measures the annual pre-tax cash flow generated relative to the cash invested in a property. Also referred to as a cash-on-cash yield, it is calculated by dividing the annual net cash flow (after debt service) by the equity invested. This metric is beneficial for comparing investment opportunities that utilize financing, as it reflects the return on the investor’s out-of-pocket cash, rather than the entire property value. [7]

Significance:

- Performance Indicator: It shows how efficiently an investment generates cash flow relative to the initial cash invested.

- Investment Decision Tool: This tool helps investors evaluate property investments’ liquidity and immediate profitability. It is beneficial for comparing different property investments.

In summary, the cash-on-cash return is a straightforward metric for assessing the profitability and cash flow efficiency of real estate investments based on the actual cash invested.

Equity Multiple

Equity multiple (EMx) in commercial real estate is a financial metric that compares the total cash an investor receives relative to the total amount of capital they invested. It is calculated by dividing the cash flow distributed during the holding period (including distributions and profits from a sale) by the total equity invested. So, if you invest $400,000 in a property and receive $100,000 in cash flow each year for five years, then turn around and sell the property for $1 million, your total cash would be $1.5 million. Divide 1.5 million by $400,000, and you get the equity multiple, which in this case is 3.75x. In other words, you earned $3.75 for every dollar you invested. [7]

Importance:

- Total Return: Unlike IRR or cash-on-cash return, the equity multiple provides a simple snapshot of total financial return without time value adjustments.

- Investment Assessment: It helps investors quickly gauge the overall profitability of an investment, simplifying comparisons between opportunities.

Equity multiple is a valuable tool for real estate investors to understand the total return potential of their investments relative to the equity or debt they have contributed.

When Do LPs Get Paid?

The answer to this question varies depending on the deal structure. Every syndication deal is unique, and limited partners (LPs) should conduct thorough due diligence before participating. With that said, the term “waterfall” refers to the arrangement of parties (i.e., investors, limited partners, and general partners) in their specific payout order (return of capital).

Here’s the waterfall and promote structure that Janover offers:

Say a sponsor invests 5% equity in a $1 million property ($50,000), and the pool of limited partners invests 95% ($950,000); the first contractually agreed-upon return hurdle could be a 9% IRR. Once the LPs have received their original capital and a 9% return, any remaining profits are split according to the terms of the agreement. For example, the sponsor gets 20% of the profits, and the investors receive 80%. [9]

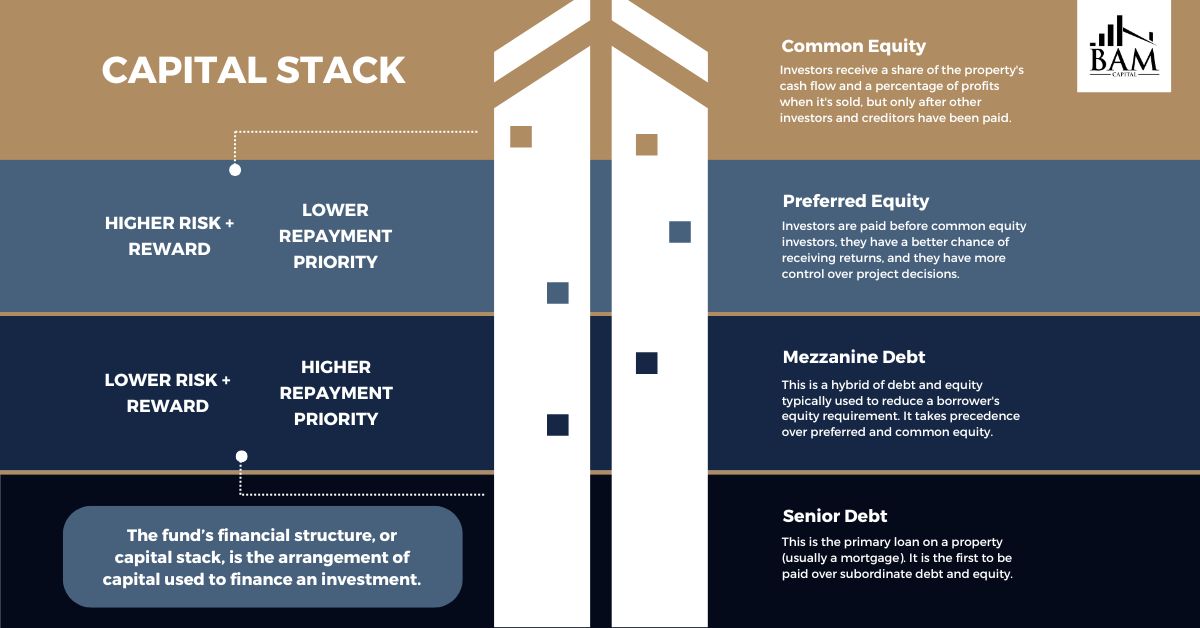

The capital stack in private placement represents the financial structure of a commercial real estate deal. It visualizes the various types of capital used to finance the project, showing the order in which investors and lenders are repaid, as well as the risk and reward associated with each layer of the capital stack. [9]

What is an Accredited Investor?

According to Rule 501 of Regulation D of the Securities Act of 1933 (Reg. D), an accredited investor is defined by the U.S. Securities and Exchange Commission (SEC) as a natural person with income that exceeds $200,000 in each of the two most recent years, with a reasonable expectation of the same level of income in the current year. For spouses, a joint income that exceeds $300,000 is required. [10]

An accredited investor may also be a natural person whose individual net worth or joint net worth with the person’s spouse exceeds $1 million. This net worth excludes the value of the person’s primary residence.

There is no accreditation process to go through. There is also no government agency or independent body that exists to provide accreditation to qualified investors. This means there is no exam or piece of paper to acquire. However, BAM Capital and other multifamily private placement (syndication) companies require proof of investors’ accredited status, which can be obtained from a letter from a potential investor’s CPA stating that they are accredited. Instead of an accreditation process, the companies that issue unregistered investments and securities are in charge of identifying a potential investor’s qualifications. Once you have met these guidelines, you can invest in securities not registered with the SEC. [10]

The SEC’s definition of accredited investors extends beyond financial qualifications to include specific professionals and additional entities. Amendments introduced on August 26, 2020, included adding registered brokers and investment advisors to the definition.

Why Accredited Investors Prefer Multifamily

Leverage

Accredited investors often gravitate towards multifamily syndications due to the potential for leveraging their investments. However, as with any tool, debt must be used appropriately to achieve the best results. Debt (or leverage) is a tool that allows investors to buy assets using less of their capital. Opportunities that would otherwise be closed off to investors become possible when using debt. The following scenario illustrates how debt can enhance returns:

Property X is a $10M property that has an NOI of $500k with 70% leverage (debt), meaning 30% of the property’s value ($3M) is equity (cash). The 5-year cash flow equals $1.1M after debt service. Property X’s value increases by $3M over the next five years (hold period), totaling your profits at $4.1M; this is your cash flow ($1.1M) plus the increased property value ($3M). You calculate your return on equity by dividing your profit by your capital investment. So, $4.1M divided by $3M equals a 137% return. This would qualify as an amplified or enhanced return. [6]

Imagine you purchased Property X with cash only, meaning you didn’t borrow any capital. 100% of Property X’s value is equity. The 5-year cash flow equals $2.5M since you have no debt service. Property X’s value increases by $3M over the next five years (hold period), totaling your profits at $5.5M; this is your cash flow ($2.5M) plus the increased property value ($3M). You calculate your return on equity by dividing your profit by your capital investment. So, $5.5M divided by $10M equals a 55% return. This detailed calculation shows how leveraging real estate can maximize your cash-on-cash return. [6]

Forced Appreciation

Forced appreciation occurs when investors actively implement physical and/or operational value-add strategies to boost the property’s net operating income (NOI) and value. Real estate properties tend to appreciate over time due to natural factors such as inflation and increased demand for housing. Natural appreciation is heavily driven by population or economic growth in desirable markets. [11] Property owners can also create forced appreciation by renovating or improving the property. When the property sells, the owner can “realize” a profit from the appreciation, increasing their cash flow. [11][12]

Cash Flow

Real estate is a cash-flow business. There are several ways in which cash flow can be generated in multifamily real estate. The most common method is through rental income. Property owners receive rental payments from residents, typically monthly. [11] The strategy is to underwrite a property not on in-place cash flow but on stabilized cash flow. Cash flow is a catch-all term typically used to describe the income a property produces after all operating expenses and debt have been paid. This includes mortgage payments, property taxes, insurance, maintenance, utilities, and property management fees. [11]

In-place cash flow:

The cash flow a property generates at the time of purchase.

Stabilized cash flow:

Projected cash flow once a property has reached its full potential in terms of occupancy and income.

Whenever you read “stabilized” attached to a metric (cash flow, NOI, etc.), understand that it is interchangeable with “projected.” For example, stabilized NOI (net operating income) is equivalent to NOI once the property has reached its market potential. As you build up your equity and pay down your mortgage, your cash flow tends to strengthen. Positive cash flow occurs when the income generated from the property exceeds the total expenses, while negative cash flow occurs when expenses surpass the income. [11]

Tax Benefits

Investing in real estate comes with many tax advantages. For example, several expenses associated with owning an investment property, such as mortgage interest, property management fees, property insurance, ongoing maintenance costs, and property taxes, can be deducted from your tax obligations. This is outlined on K-1 tax forms for passive investors in private placements. Successfully navigating balanced cash flow, capital preservation, and capital appreciation while providing risk-adjusted returns could result in long-term capital gains. [11]

Partnerships can also lead to tax advantages by sharing costs. A partnership in multifamily real estate can take several different forms. One typical partnership structure involves a developer, a company managing the construction of a commercial multifamily property, and an owner/operator. The partnership is called a joint-venture development deal. Joint-venture development deals can add value to the property and the parties involved. They promote the development of new multifamily communities and address the supply/demand imbalance currently happening nationwide. In other words, developers might have a lot of deliveries (completed properties) today, but shovel-ready (under construction) projects could be much higher. [11]

Investors can deduct the cost of acquiring and improving rental property over time through depreciation, a non-cash deduction allowing real estate investors to write off a property’s cost over 27.5 years for residential and 39 years for commercial properties. Investors can even depreciate improvements made to the property to enjoy more tax benefits. [11]

Investors can also defer taxes through a 1031 exchange, which allows investors to sell a property and reinvest the proceeds into another like-kind property without immediately paying capital gains taxes on the sale. By deferring these taxes, real estate investors can leverage their capital more effectively, increasing their potential return on investment (ROI). [11]

In a private placement, however, investors may not be eligible for a 1031 exchange. Remember, private placement in multifamily is a real estate deal where multiple investors pool their money to purchase a property, typically an apartment building, condominium, or townhouse (also known as multifamily). The investors are led by a general partner, also known as a sponsor, who is responsible for finding the property, managing the transaction, and overseeing the property after the purchase. Funds can be structured as partnerships, corporations, or trusts. [11]

So, investors cannot typically 1031 into a fund because the structure of a fund may not give limited partners (LPs) ownership of an asset; instead, they have limited shares or interest in a fund, which does not qualify as a “like-kind” property. In other words, investors cannot directly exchange property for shares in a fund. Specific funds are structured to meet the requirements of 1031 exchanges (e.g., Delaware Statutory Trusts (DSTs)). [11][13]

Diversification

Diversification in investment real estate comprises spreading investments across various property types, locations, and markets. This strategy aims to reduce the risk of losses by ensuring that no single investment or asset is excessively dependent. Managing several units in one building is much easier than managing several scattered-site residences. [13]

Earlier, we addressed how multifamily can offer more consistent cash flow. This is because in multifamily, you have considerable latitude in paying the bills if a few residents are delinquent. With single-family, there is zero rent if the resident does not pay their rent. Finally, cash flow is typically lower with single-family residences due to the single source of income. [13]

How to Choose the Right Syndicator

Several red flags can indicate a less-than-ideal investment when evaluating a multifamily private placement. [14] Choosing the right syndicator for your multifamily syndication is necessary for the success of your investment. Here are some guidelines on how to evaluate potential syndicators:

Reputation & Testimonials

A syndicator’s reputation reflects their track record, integrity, and ability to deliver. Look for syndicators with a proven history of successful deals, transparent communication, and ethical practices.

Testimonials from previous investors offer valuable insights into the syndicator’s performance, professionalism, and reliability. Look for reviews online and feedback from those with firsthand experience working with the syndicator. This will allow you to gauge their level of satisfaction.

Metrics

For passive investors, overly optimistic or inaccurate metrics can serve as red flags before investing. For example, if the property’s vacancy and turnover rates are high, this could indicate operational deficiencies and/or an underperforming market. In that context, if the sponsor targets 99% occupancy in a market with little job or population growth, that should give investors pause. Similarly, the property may lack upgraded amenities, but it should raise questions if the sponsor anticipates a 10% rental rate growth with no clear plan to justify such increases. Does the sponsor’s plan to completely renovate the property to attract higher-paying residents make sense if the area’s job market is weak? [14]

Consider the number of deals they’ve successfully closed, the performance of those deals in terms of returns to investors, and their ability to navigate various market conditions. A strong track record instills confidence that the syndicator has the expertise and competence to execute their investment strategy effectively and deliver favorable outcomes.

Financial Stake

Financial Stake

A syndicator’s risk appetite can significantly impact the investment strategy, determining whether it will pursue conservative, moderate, or aggressive approaches. It’s crucial to align their risk tolerance with your investment objectives and comfort level.

Financial stake is commonly referred to as “skin in the game” in real estate jargon and refers to the amount of cash the sponsor has invested in the deal. Determining whether the sponsor’s stake is sufficient will be up to your unique perspective. Still, generally speaking, a well-founded sponsor with a dependable track record will invest anywhere from 5% to 20% of the total equity necessary for a deal. Sometimes, a sponsor’s stake is less in equity and more in debt recourse. Recourse debt refers to loans wherein the lender is legally allowed to collect what is owed for the debt even after taking collateral (e.g., a property). [14]

Is Investing In a Multifamily Syndication Right for You?

Investing in a multifamily syndication can be a compelling option for accredited investors seeking passive income and portfolio diversification. However, multifamily properties can be expensive, making them more challenging for individual investors to acquire. This fact, along with the eligibility requirements, can limit the pool of potential investors in private placements. Private placements are typically only available to accredited investors; however, non-accredited investors may be able to invest in select real estate investment trusts (REITs) or crowdfunding endeavors. [15]

Remember, the period during a real estate lifecycle when a sponsor owns or “holds” a property before selling it is called the hold period. Since these investments are illiquid, investors should expect their capital in a private placement deal to be tied up for several years as the sponsor holds assets to generate returns through forced and natural appreciation. [15] LPs should be comfortable with the illiquidity aspects of a multifamily investment.

Multifamily private placements are designed to address the challenges of direct ownership by providing investors with all the benefits of multifamily investment properties without the burden or physical labor of managing these properties directly. This structure allows access to institutional-quality real estate while the sponsor handles all the work. It can be a strategic approach if you want to invest in real estate but also want a passive role. [15]

Regardless of the type of investment, investors should always consider their risk tolerance, investment goals, and liquidity needs before committing capital. This also applies to multifamily syndication. Perform your due diligence before participating in any type of investment.

Why Choose BAM Capital?

We have discussed the importance of a reputable track record when choosing a syndicator. Accredited investors who want to work with a syndicator with a reliable track record for excellence should work with BAM Capital.

What is BAM Capital?

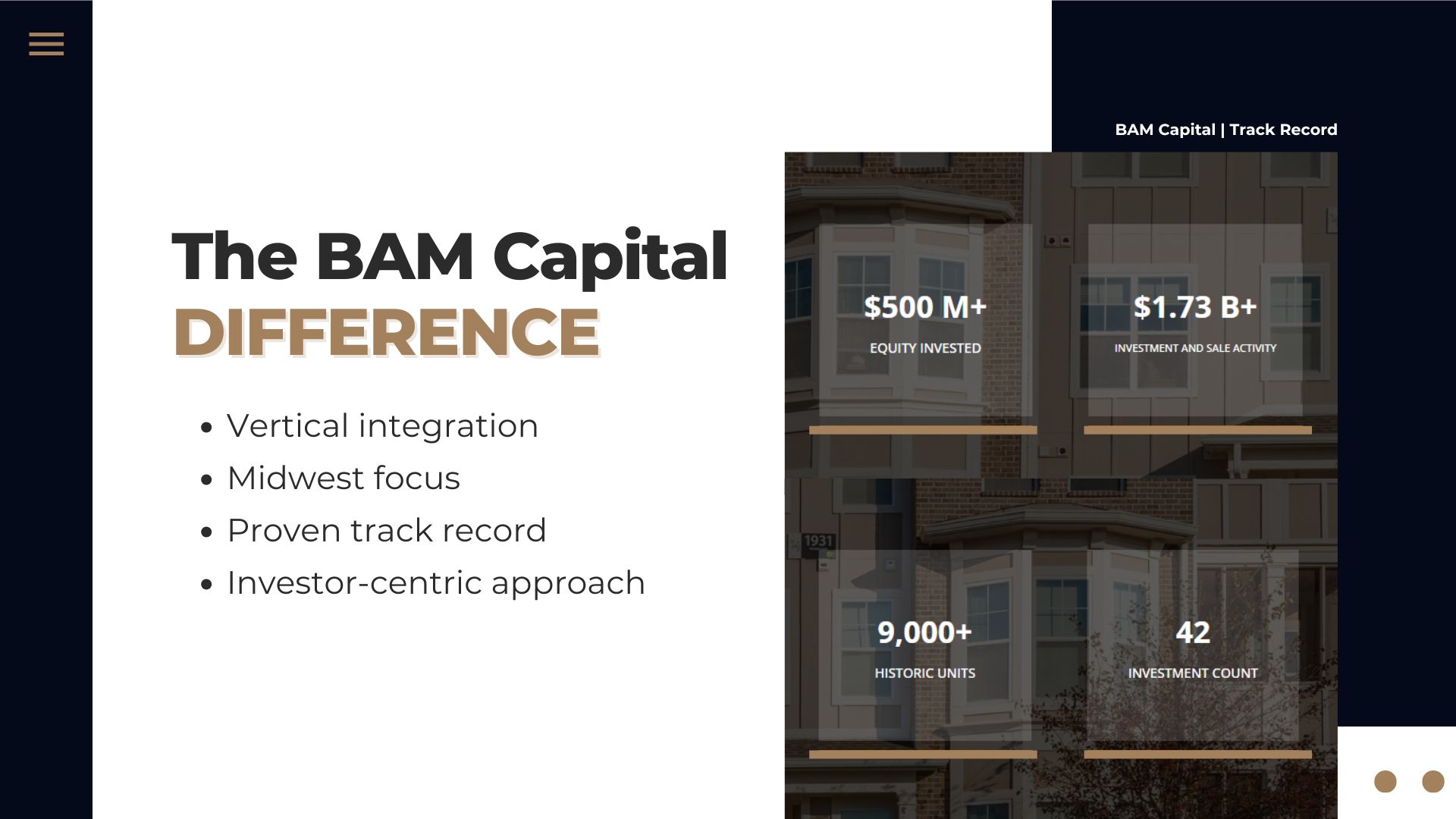

Based in Indianapolis, Indiana, The BAM Companies is a vertically integrated multifamily real estate company controlling multiple stages of the investment cycle through its business divisions: BAM Capital, BAM Management, and BAM Construction. Said succinctly, the organization owns and operates institutional-quality, market-rate apartment communities situated in locations where demand outpaces supply and are characterized by major economic drivers, quality schools, and upscale retail. Since its inception, BAM Capital has executed more than $1.7 billion in multifamily real estate transactions. Finding these opportunities is one thing, but capitalizing on them is The BAM Companies’ core competency and a direct path to building generational wealth for its investors. [16]

What is the firm’s track record?

BAM Capital has consistently provided above-average, risk-adjusted returns to its investors. For example, the firm has achieved an internal rate of return (IRR) of 33.4% and an equity multiple of 2.46x over a 3.5-year investment hold period—impressive statistics that reflect operational expertise rather than market timing. BAM Capital has gone full-cycle (acquire, manage/execute, and sell) on many apartment communities. Multifamily investment has stood the test of time through multiple adverse economic downturns and is battle-tested. This consistent performance is a testament to the resilience of the multifamily asset class and the prowess of an effective owner/operator like The BAM Companies. [16]

How does BAM Capital source multifamily investment opportunities?

BAM Capital has developed a credible reputation over the years. This reputation encompasses the organization’s unwavering commitment to integrity, which breeds compelling investment opportunities for industry experts, including investment sales brokers and real estate owners. Not only is reputation important, but BAM Capital is more proactive than reactive when seeking potential investment opportunities. Our team refers to it as the “battle rhythm,” a term typically used in a military context. However, the term characterizes our team’s approach to uncovering opportunities through consistent and constant communication with the investment community. It also ensures effective performance and allows the firm to act swiftly when market conditions change. BAM Capital’s exceptional reputation and proactive mentality are a recipe for long-term success. [16]

- BAM Capital utilizes a conservative approach to leverage, a key attribute of prudent borrowers.

- The firm views the stabilized yield on cost as the most critical metric in real estate valuation, turning negative leverage into positive leverage.

- Interest rate derivatives, such as rate caps, and their impact during interest rate volatility are significant hedges.

- Prepayment flexibility is of utmost importance. It allows borrowers to pivot with a refinance or sale after executing the asset’s business plan without a costly prepayment penalty. [16]

BAM Capital partners with accredited investors who want to enjoy passive income and all the other benefits of multifamily private placement. As the private equity arm of The BAM Companies, BAM Capital has been focusing on buying the most profitable assets and staying disciplined in its investment thesis. BAM Capital’s investment strategy aims to create forced appreciation while mitigating investor risk. To date, the brand has successfully managed over $1.7 billion in assets across ~9,000 apartment units.

Remember that no investment is without risk. Before making financial decisions, consult your investment advisor and schedule a call with a BAM Capital investment team member.

For additional multifamily real estate insights, visit Pathways to Passive Wealth, BAM Capital’s new platform designed to make real estate investing more accessible, transparent, and achievable for aspiring and experienced investors.

Sources:

[1]: BAM Capital. (2025). “How do I start multifamily real estate investing?” https://bamcapital.com/start-multifamily-real-estate-investing/

[2]: BAM Capital. (2025). “The importance of partnerships in multifamily real estate.” https://bamcapital.com/the-importance-of-partnerships-in-multifamily-real-estate/

[3]: Investopedia. (2025). “Are Real Estate Syndicates a Good Investment?” https://www.investopedia.com/are-real-estate-syndicates-a-good-investment-8416965

[4]: Multifamily Refinance. (2023). “Multifamily Syndication: The Complete Guide.” https://www.multifamilyrefinance.com/apartment-investing-blog/multifamily-syndication#css

[5]: Pathways to Passive Wealth. (2025). “Topic 4.1 | The Role of Sponsors in Multifamily Investments.” https://learn.bamcapital.com/courses/multifamily-real-estate/lessons/topic-4-the-mechanics-of-multifamily-private-placement-investing/topics/topic-4-1-the-role-of-sponsors-in-multifamily-investments/

[6]: Pathways to Passive Wealth. (2025). “Topic 2.4 | Financing Multifamily Properties.” https://learn.bamcapital.com/courses/multifamily-real-estate/lessons/topic-2-how-multifamily-real-estate-works/topics/topic-2-4-financing-multifamily-properties/

[7]: Pathways to Passive Wealth. (2025). “Topic 3.1 | Key Metrics for Investors.” https://learn.bamcapital.com/courses/multifamily-real-estate/lessons/topic-3-evaluating-multifamily-investments/topics/topic-3-1-key-metrics-for-investors/

[8]: BAM Capital. (2023). “What is IRR in real estate & how is it determined?” https://bamcapital.com/what-is-irr-in-real-estate/

[9]: Pathways to Passive Wealth. (2025). “Topic 4.3 | Understanding Private Placement Structures.” https://learn.bamcapital.com/courses/multifamily-real-estate/lessons/topic-4-the-mechanics-of-multifamily-private-placement-investing/topics/topic-4-3-understanding-private-placement-structures/

[10]: BAM Capital. (2025). “How to become an accredited investor: Step-by-step.” https://bamcapital.com/how-to-become-an-accredited-investor-step-by-step/

[11]: Pathways to Passive Wealth. (2025). “Topic 1.3 | Foundations of Building Wealth with Multifamily Real Estate.” https://learn.bamcapital.com/courses/multifamily-real-estate/lessons/topic-1-introduction-to-multifamily-real-estate/topics/part-3-foundations-of-building-wealth-with-multifamily-real-estate/

[12]: BAM Capital. (2025). “How to become an accredited investor: Step-by-step.” https://bamcapital.com/accredited-investor-step-by-step/

[13]: Pathways to Passive Wealth. (2025). “Topic 1.2 | Why is Multifamily Real Estate a Strong Investment?” https://learn.bamcapital.com/courses/multifamily-real-estate/lessons/topic-1-introduction-to-multifamily-real-estate/topics/part-2-why-is-multifamily-real-estate-a-strong-investment/

[14]: Pathways to Passive Wealth. (2025). “Topic 4.4 | How to Evaluate a Multifamily Private Placement Investment.” https://learn.bamcapital.com/courses/multifamily-real-estate/lessons/topic-4-the-mechanics-of-multifamily-private-placement-investing/topics/topic-4-4-how-to-evaluate-a-multifamily-private-placement-investment/

[15]: BAM Capital. (2025). “What is private placement?” https://bamcapital.com/what-is-private-placement/

[16]: BAM Capital. (2025). “The BAM Capital Way.” Written by Tony Landa.