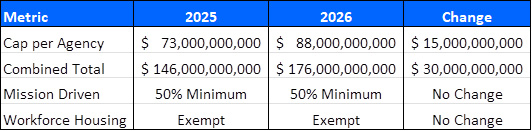

In November 2025, the FHFA announced a significant increase in the multifamily loan purchase caps for Fannie Mae and Freddie Mac for the 2026 calendar year. For 2026, the loan purchase caps are set at $88 billion for each Enterprise, resulting in a combined total of $176 billion in lending capacity. The 2026 limits represent a 20.5% increase over the 2025 levels, reflecting an expectation of much higher transaction activity.

Key Policy Highlights

- Mission-Driven Focus: “Mission-Driven” refers to a regulatory requirement set by the FHFA that mandates Fannie Mae and Freddie Mac to focus their capital on affordable housing and underserved markets. For 2026, the FHFA requires that at least 50% of all multifamily loans purchased by the agencies must meet these “mission-driven” criteria. This requirement ensures the agencies prioritize the housing needs of low-to-moderate-income families rather than simply luxury communities.

- Workforce Housing Exemption: Essentially, if a loan meets “Workforce Housing” criteria, it does not utilize any of the $88 billion limit for that agency. This creates an uncapped pool of capital for properties that cater to middle-income renters like teachers, police officers, and healthcare workers.

Why This Is Important

By raising the combined limit for Fannie Mae and Freddie Mac to $176 billion, the FHFA is signaling a rise in transaction activity while also looking to stabilize a market facing a unique set of pressures. The increase in lending caps is a major signal to multifamily real estate owners and investors for several reasons.

- Addressing the “Maturity Wall”: The industry estimates that the maturing debt for multifamily in 2026 will fall between $90 billion and $162 billion, depending on the source and whether “extended” loans from previous years are included. These maturities will be closely watched by economists and investors as many of these loans originated during the low-interest-rate environment will now face significantly higher refinancing costs. The increased caps help to ensure there is enough liquidity for owners to refinance their properties.

- Improving Market Confidence: A 20% increase in lending capacity is a public bet by the government that transaction volume will increase. This encourages private equity and institutional investors to start buying again. The additional lending capacity by Fannie Mae and Freddie Mac creates a more predictable environment for private capital to return, as it signals a belief that interest rates are stabilizing, and property values have found their “bottom.”

- Providing Counter-Cyclical Support: In the financial world, the term “counter-cyclical” means moving in the opposite direction of the general economic cycle. For Fannie Mae and Freddie Mac (the GSEs), providing counter-cyclical support means the GSE’s ensure that money is still available for mortgages even when the rest of the economy is in a tailspin. When private banks or CMBS lenders become conservative, the GSE’s step up to prevent a credit crunch. These higher caps provide an additional cushion to support the market if private capital remains on the sidelines.

- Incentivizing Affordability: Lending from the GSEs, specifically Fannie Mae and Freddie Mac, incentivizes affordability by passing “pricing benefits” down the chain from the lender to the property owner, and ultimately to the resident. For example, if an owner wants to obtain a lower interest rate, the borrower or owner must cap rents at a specific percentage of the Area Median Income (AMI). The purpose is to ensure that residents like teachers or nurses aren’t priced out of their neighborhoods.

Fannie Mae and Freddie Mac are the backbone of the multifamily lending industry. Without them, the apartment market would be significantly more volatile, more expensive for renters, and prone to “freezing” during economic downturns. Unlike private banks or Wall Street investors, Fannie and Freddie have a federal mandate to provide capital in all economic cycles. This federal mandate is the primary reason the multifamily sector is more liquid and the “buyer universe” is much larger than other real estate asset classes.

Disclaimer: This document is for informational purposes only and is not financial, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital are made pursuant to Rule 506(c) of Regulation D and are available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC). Verification of accredited investor status is required before participation in any investment. The information contained herein reflects the opinions of the author and does not necessarily represent the views of BAM Capital. Any financial terms, projections, or forward-looking statements contained herein are hypothetical in nature and should not be interpreted as guarantees of future performance or safety. Such statements reflect opinions and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including but not limited to illiquidity, economic downturns, and potential loss of invested funds. Past performance does not guarantee future results. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions. The information provided in this article is current as of its publication date, September 2025. BAM Capital makes no representation or warranty regarding the accuracy or completeness of the information contained herein.

© 2026 BAM Capital. All rights reserved.

Author: Tony Landa, Senior Economic Advisor, The BAM Companies, February 2026