Acquired 12/2025

PCF & Fund V

Kinsley Forest

Kansas City, MO

328

Units

15-20%

Targeted IRR

2.0x-2.5x

Targeted Equity Multiple

History doesn’t repeat itself, but it rhymes — and right now it’s rhyming loudly with the mid-to-late 1940s. In 1946, the United States emerged from World War II with federal debt at 106% of GDP, the highest in its history. This year, for the first time since that era, debt held by the public crossed 100% of GDP again, and the Congressional Budget Office projects it will reach 120% within a decade. Layer on political fracture and income inequality at levels last seen around the war years, and the parallel becomes hard to ignore.

The question that matters for investors isn’t whether Washington will deal with this debt. It’s how. And the last time America faced this exact problem, the answer wasn’t austerity, default, or a miracle of growth. It was the Federal Reserve — quietly, deliberately, and at the expense of anyone holding bonds and cash.

Debt. The 1946 peak of 106% came from a war that had ended; the bills stopped arriving. Today’s 100% comes with peacetime deficits running north of 6% of GDP and entitlement spending that compounds on autopilot. In one sense, our position is more challenging than 1946 — the borrowing hasn’t stopped.

Division. We tend to remember the late 1940s through a sepia filter of unity, but Americans living through it experienced something closer to chaos. In 1946, roughly five million workers walked off the job in the largest strike wave in U.S. history. Inflation hit double digits as price controls came off. Truman waged open war with what he called the “Do-Nothing Congress,” and the first loyalty scares that became McCarthyism were already brewing. Distrust in institutions, anger over the cost of living, fights between labor and capital — it all sounds familiar.

Inequality. Before the war, the top 1% of Americans earned more than 20% of national income. The 1940s produced what economists call the Great Compression — a dramatic flattening driven by wartime wage controls, confiscatory top tax rates, surging union membership, and inflation that quietly devalued old fortunes. Today, the top 1% share has round-tripped back above 20%, union membership has fallen from over 30% of the workforce to roughly 10%, and the political pressure that builds in such conditions is visible everywhere.

From 1942 to 1951, the Federal Reserve didn’t set interest rates the way we think of today — it pegged them. Treasury bills were capped at 0.375% and the long bond at 2.5%, and the Fed bought whatever quantity of government debt was necessary to hold those ceilings. Call it what it was: debt monetization in service of the Treasury. The central bank was, for nearly a decade, an arm of war finance.

Then came the crucial part. When price controls lifted in 1946, inflation surged — 8% in 1946, north of 14% in 1947 — while the Fed held nominal rates pinned near zero on the short end. Real interest rates went deeply negative. Every saver holding a Treasury bond or a bank deposit earned a yield far below inflation, year after year. Economists call this financial repression. It is a wealth transfer from lenders to borrowers, and the borrower-in-chief was the U.S. government.

It worked. Debt-to-GDP fell from 106% in 1946 to 23% by 1974. The comfortable story is that America “grew its way out.” The data says otherwise: recent IMF and NBER research decomposing that decline finds that growth alone would have taken the ratio only from 106% to about 74%. The majority of the heavy lifting came from primary surpluses, surprise inflation, and interest-rate distortion — the Fed holding rates below inflation. Bondholders paid down the war debt without ever receiving a default notice. The arrangement lasted until the Treasury-Fed Accord of March 1951 restored the Fed’s independence — but only after the repression had done its work.

The 1940s analog isn’t just monetary — it’s industrial. Postwar America converted its war machine into the world’s dominant manufacturing base, and when Washington wanted to build at scale, it reached for the language of national security. The 1956 highway bill that built the interstate system was formally titled the National Interstate and Defense Highways Act. Defense was the political wrapper around a generational infrastructure buildout.

That template is back. The FY2027 defense request of roughly $1.5 trillion — on top of a record $1 trillion for FY2026 — represents the largest defense ramp since the Korean War, with massive line items for shipbuilding, munitions production, and the “Golden Dome” missile defense program. The CHIPS Act has catalyzed more than $630 billion of announced semiconductor investment across 140 projects. Real manufacturing construction spending has more than doubled since 2021. The Pentagon is directly funding rare-earth magnet plants and lithium mines to rebuild domestic supply chains. Reshoring initiatives tracked roughly a quarter-million announced manufacturing jobs in 2024 alone.

Strip away the program names and you have the 1940s formula: government-directed capital flooding into factories, energy, logistics, and defense infrastructure — spending that is structural, politically durable because it wears a national-security badge, and inherently inflationary because it consumes real resources, labor, and materials.

Here is the uncomfortable arithmetic: net interest on the federal debt now rivals the defense budget itself. At today’s debt levels, every percentage point of interest rates costs the Treasury hundreds of billions per year. No Congress of either party will run the multi-trillion-dollar surpluses needed to pay debt down honestly, and outright default is unthinkable. That leaves one historically proven exit — the 1940s one: hold nominal rates below inflation and let the debt melt in real terms.

I don’t expect the Fed to announce formal yield curve control with a press release. I expect it by increments, and the increments have arguably begun. Quantitative tightening ended in December 2025, and the Fed is again buying roughly $40 billion of Treasury bills per month — framed as “reserve management,” but mechanically indistinguishable from monetizing a portion of new issuance. A new Fed chair has taken office under a president openly demanding lower rates. Bank regulation is being reshaped in ways that encourage institutions to hold more Treasuries. The Treasury itself is leaning on short-dated issuance the Fed can most easily absorb. Each step is defensible in isolation; together they trace the outline of fiscal dominance — monetary policy gradually subordinated to the government’s financing needs, exactly as it was from 1942 to 1951.

The likely end state: inflation that runs persistently in the 3–4% range while policy rates and long yields are managed below where free markets would set them. Not hyperinflation — the 1940s never saw that either. Just a decade or more of quietly negative real rates doing silent, compounding work on the debt ratio. The savers of the late 1940s never got a vote, and neither will today’s.

Financial repression is a transfer from lenders to borrowers. Position yourself on the right side of that transfer.

The designated losers are long-dated nominal bonds and cash. From the mid-1940s through the bond bear market that followed, Treasury holders lost more than half their purchasing power in real terms — the era that earned bonds the nickname “certificates of confiscation.” If the playbook repeats, the 60/40 portfolio’s ballast becomes its anchor.

The winners are productive hard assets whose income rises with inflation — and especially those that can be financed with long-term, fixed-rate debt. Income-producing real estate is doubly advantaged in this regime: rents and replacement costs ride inflation upward while the real value of the mortgage erodes — the investor becomes a beneficiary of the same repression that punishes the bondholder. Housing in particular sits at the intersection of inflation protection and a structural national shortage. Beyond real estate, the reindustrialization wave creates a tailwind for industrial property, energy, infrastructure, and the communities surrounding reshoring corridors, where hundreds of billions in factory investment translate into jobs, wages, and housing demand.

The honest caveats: history rhymes, it doesn’t repeat. An AI-driven productivity boom could lift growth enough to soften the arithmetic, or a genuine austerity turn in Washington could change the path. And none of this is investment advice — it’s a framework. But when I look at debt at World War II levels, a Fed balance sheet growing again, the largest defense buildup since Korea, and factories rising across the heartland for the first time in two generations, I see 1946 — and I’d rather own the assets that era rewarded than the paper it quietly confiscated.

Ivan Barratt

Founder & CEO

The BAM Companies

This article reflects the author’s opinions and is provided for informational purposes only; it does not constitute investment, legal, or tax advice.

Syndications and funds are often used interchangeably in multifamily real estate, but they are structured differently and offer distinct experiences for investors, even though both provide access to the asset class.

In a traditional syndication, investors typically place capital into a single, specific property. That means you can review the individual asset, the market, and the business plan before deciding whether to invest.

A fund works differently: your capital is pooled and allocated across multiple investments selected by the sponsor. While this involves risks related to the sponsor’s discretion and fund-level administrative expenses, a fund can also leverage economies of scale—such as consolidated legal, accounting, and operational costs—spread across a broader portfolio.

The difference often comes down to what matters most to you.

A syndication can offer:

A fund can offer:

With a fund, you may not need to evaluate every deal yourself, but that also means placing more trust in the sponsor making those decisions for you.

That is why experience, discipline, and operational quality matter even more in a fund structure.

For investors who want passive exposure without reviewing every opportunity individually, a fund can provide a simpler way to invest.

If you would like to see how BAM Capital’s fund structure works, request access to the Fund Offering Memorandum to review the strategy in more detail.

Disclaimer: This content is for informational purposes only and is not financial, tax, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital and its affiliates are made pursuant to Rule 506(c) of Regulation D, available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers, as defined by Section 2(a)(51) of the Investment Company Act of 1940. Verification of accredited investor status is required before participation in any investment.

Contact BAM Capital for details on current offerings. BAM Capital and its representatives are not fiduciaries or investment advisors. The information provided is general and may not reflect individual financial goals. Financial terms, projections, or forward-looking statements contained herein are hypothetical and should not be interpreted as guarantees of future performance or safety. Such statements reflect BAM Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including, without limitation, illiquidity, economic downturns, and potential loss of invested funds or capital. Past performance does not predict or guarantee future results. Historical transaction figures represent past performance across multiple deals as of the date this information was published, not a single investment transaction. BAM Capital and its affiliates do not guarantee the accuracy or completeness of this information. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2026 BAM Capital. All rights reserved.

One of the reasons some investors hesitate before making their first passive real estate investment is uncertainty about what to expect at tax time.

They have heard about K-1s, depreciation, and paper losses, but the reporting can feel unfamiliar at first.

The good news is that a K-1 is usually much simpler than it seems once you understand what it is showing.

When you invest in a private real estate fund as a limited partner, you are typically investing through a partnership structure, which means you receive an IRS Schedule K-1 instead of a 1099. This form is generated from the partnership’s annual tax return (Form 1065) and reports your share of the entity’s income, deductions, and credits for the year.

Your CPA or tax professional will use the information on your Schedule K-1 to prepare your personal tax return. You don’t need to file the K-1 separately. Instead, the form reports your share of the multifamily property’s income, depreciation-related deductions, losses, and other tax items, which are incorporated into your individual tax return.

Every K-1 can look a little different, but a few sections usually matter most to investors:

For many investors, the most surprising part is that a property can generate cash distributions while still showing a taxable loss on paper because of depreciation.

Real estate allows investors to depreciate the value of the property over time. Those depreciation deductions often flow through the K-1 and can help offset passive income from other real estate investments.

That means your K-1 can also give you a clearer picture of how your investment is performing behind the scenes.

K-1s are typically issued after year-end once the partnership’s reporting is complete. At BAM Capital, our team works to provide investor reporting as clearly as possible so you understand what you are receiving and when to expect it.

For many investors, the first K-1 feels unfamiliar. After that, it often becomes one of the most useful documents they receive all year.

If you’d like to better understand how tax reporting works within a private real estate fund, reach out to the BAM Capital investor relations team at invest@bamcapital.com to discuss your questions and learn how it may apply to your investment strategy.

Disclaimer: This content is for informational purposes only and is not financial, tax, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital and its affiliates are made pursuant to Rule 506(c) of Regulation D, available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers, as defined by Section 2(a)(51) of the Investment Company Act of 1940. Verification of accredited investor status is required before participation in any investment.

Contact BAM Capital for details on current offerings. BAM Capital and its representatives are not fiduciaries or investment advisors. The information provided is general and may not reflect individual financial goals. Financial terms, projections, or forward-looking statements contained herein are hypothetical and should not be interpreted as guarantees of future performance or safety. Such statements reflect BAM Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including, without limitation, illiquidity, economic downturns, and potential loss of invested funds or capital. Past performance does not predict or guarantee future results. Historical transaction figures represent past performance across multiple deals as of the date this information was published, not a single investment transaction. BAM Capital and its affiliates do not guarantee the accuracy or completeness of this information. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2026 BAM Capital. All rights reserved.

The BAM Companies is proud to announce that it has earned the prestigious 2026 USA TODAY Top Workplaces award. The BAM Companies also received this award in 2023, 2024, and 2025.

The award honors organizations with 150 or more employees that have created exceptional, people-first cultures. This year, more than 40,500 organizations were invited to participate. The winners are recognized for their commitment to fostering a workplace environment that values employee listening and engagement. USA TODAY showcased the winners online and at the National Awards Summit in Nashville.

Additionally, The BAM Companies was named to USA TODAY’s Purpose & Values Top Workplaces, Compensation & Benefits Top Workplaces, Work-Life Flexibility Top Workplaces, Leadership Top Workplaces, Innovation Top Workplaces, Employee Well-Being Top Workplaces, Top Workplaces for Appreciation, Professional Development Top Workplaces, and Real Estate Top Workplaces.

"A company is only as good as its people,” said Emilee Meyers, The BAM Companies COO. “You can have a great strategy, a great product, and great ideas, but none of it matters without great people behind it. What makes me most proud isn’t the award itself—it’s that we’ve built a place where talented people want to show up, contribute, grow, and do meaningful work together. We don’t take recognition like this from USA TODAY for granted. Every person on this team had a hand in earning it. And maybe I’m biased, but I’d take this team over any other. Every day of the week. The best things we’ve accomplished are a direct result of the people who make The BAM Companies what it is, and the future is exciting because they’re the ones helping build it.”

The winners are determined by authentic employee feedback captured through a confidential survey conducted by Energage, the HR research and technology company behind the Top Workplaces program since 2006. The results are calculated based on employee responses to statements about Workplace Experience Themes, which are proven indicators of high performance.

“Earning a USA TODAY Top Workplaces award is a testament to an organization’s credibility and commitment to a people-first culture," said Eric Rubino, CEO of Energage. "This award, driven by real employee feedback, is more than just a recognition — it’s proof that your employees believe in the organization and its leadership. Job seekers and customers look for this trusted badge of credibility and excellence. It signals a company that values its people, and that kind of culture resonates in today’s competitive market”

About The BAM Companies

Headquartered in Carmel, Indiana, The BAM Companies specializes in the acquisition and management of multifamily apartment communities. Comprising BAM Capital, BAM Management, and BAM Construction, The BAM Companies has been named as the Indiana Apartment Association’s 2024 Management Company of the Year, a Top Workplace by IndyStar for four consecutive years, a recipient of the Indianapolis Business Journal’s Fast 25 award, and is one of Inc.’s 5000 fastest-growing private companies in America for the last eight consecutive years.

If you’ve spent any time evaluating real estate investments, you’ve likely encountered two metrics repeatedly: Internal Rate of Return (IRR) and equity multiple.

When weighing equity multiple vs IRR, it’s important to remember that while both measure returns, they tell very different stories about a deal’s performance. Understanding this distinction is essential for evaluating investments with clarity and confidence.

By seeing how IRR and equity multiple (also known as MOIC, or multiple on invested capital) work together, you can set more realistic expectations, make informed decisions, and avoid relying on single numbers that only tell part of the story.

At its core, IRR measures the velocity of your money. While the technical definition is the discount rate that brings the net present value (NPV) of all cash flows to zero, in practical terms, IRR shows the compounded annual rate at which your capital grows over the life of an investment.

Because of the time value of money, a dollar earned in year one is generally more valuable than a dollar earned in year five—and IRR accounts for that by placing greater weight on earlier cash flows.

Beyond timing, IRR incorporates both ongoing income and sale proceeds, expressed as an annualized percentage. Unlike total ROI, which measures overall gain regardless of time, IRR shows how efficiently your capital is working on a yearly basis.

In real estate investing, IRR is typically measured over a multi-year hold—often 3 to 7 years—reflecting the full lifecycle of a deal from acquisition through exit.

It’s important to note that IRR relies on projected cash flows and is highly sensitive to underlying assumptions, meaning its accuracy is only as good as the data behind it. While it reflects the timing of returns, it is most powerful when paired with metrics like the equity multiple to see the full picture of value creation.

Equity multiple measures the total cash returned relative to the amount invested over the life of a deal.

Formula:

Equity Multiple = Total Cash Returned / Total Invested Capital

Examples:

It does not matter whether that return occurs over two years or 10—equity multiple focuses purely on total capital returned. Because of this, a higher multiple over a longer hold period may appear attractive, but it does not account for how long your capital is tied up.

What equity multiple tells you:

Because it does not account for the time value of money, equity multiple is best used alongside IRR to evaluate both total return and timing. This is a key distinction in any MOIC vs IRR comparison.

There is no universal benchmark, as returns depend on strategy, risk profile, and hold period. In multifamily real estate, many investors target IRRs in the mid-teens to low-20 percent range, along with equity multiples between roughly 1.8x and 2.5x.

Some investors may pursue higher IRRs, while others prioritize more stable returns over a longer hold period.

An experienced general sponsor can meaningfully influence a deal’s performance. BAM Capital stands out from many real estate syndications by taking a vertically integrated approach, managing everything in-house from acquisition and legal oversight to operations. This structure helps ensure disciplined execution of the business plan and supports more consistent, risk-adjusted outcomes over time.

Looking at actual performance helps put this into perspective. Across a portfolio of realized multifamily assets from BAM Capital, historical results have averaged a 2.36x Net equity multiple and a 32.19% Net IRR. This consistent track record reflects our commitment to targeting strong returns and efficient timelines, keeping in mind that past success does not guarantee future results and all investments carry a risk of loss.

When evaluating real estate deals, IRR and equity multiple are most powerful when used as complementary tools. While IRR measures the speed of your return, the equity multiple confirms the total wealth created. Understanding how equity multiple vs IRR work together helps investors balance return speed with total wealth creation.

If you’re ready to see how these metrics apply to real-world multifamily opportunities, the investor relations team at BAM Capital can walk you through our current offerings and help you evaluate how they align with your portfolio goals.

Disclaimer: This content is for informational purposes only and is not financial, tax, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital and its affiliates are made pursuant to Rule 506(c) of Regulation D, available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers, as defined by Section 2(a)(51) of the Investment Company Act of 1940. Verification of accredited investor status is required before participation in any investment.

Contact BAM Capital for details on current offerings. BAM Capital and its representatives are not fiduciaries or investment advisors. The information provided is general and may not reflect individual financial goals. Financial terms, projections, or forward-looking statements contained herein are hypothetical and should not be interpreted as guarantees of future performance or safety. Such statements reflect BAM Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including, without limitation, illiquidity, economic downturns, and potential loss of invested funds or capital. Past performance does not predict or guarantee future results. Historical transaction figures represent past performance across multiple deals as of the date this information was published, not a single investment transaction. BAM Capital and its affiliates do not guarantee the accuracy or completeness of this information. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2026 BAM Capital. All rights reserved.

Owning investment property has historically been a path to long-term wealth, but it can also lead to burnout — especially for accidental landlords who never intended to manage rental property in the first place. When you’re managing multiple properties across different locations, the dream of “passive income” often starts to feel like a demanding second job.

Late-night maintenance calls, frequent tenant turnover, and tracking down rent payments can quickly turn what started as a simple investment into an operational headache. If this sounds familiar, it may be time to rethink your role.

Moving from active landlord to passive investor in multifamily properties allows you to keep the financial upside while stepping away from daily responsibilities. That’s where BAM Capital comes in. Partnering with our vertically integrated team gives you access to professionally managed, institutional-quality apartment communities across the stable Midwest market. We handle the complex logistics so you can enjoy a more passive, hands-off investment experience.

Most investors start with rental properties because of the sense of control if offers. You choose the asset, the location, and the overall strategy, and you have influence over tenant selection and management. At first, the benefits are clear and compelling:

However, as many accidental landlords eventually discover, these benefits can come with significant operational tradeoffs. The reality of maintaining a small portfolio often means:

When a small portfolio starts taking more time than it returns, the question evolves from “Is this property profitable?” to “Is this worth my time?” That is often the moment investors shift from active vs passive investing in real estate, moving from hands-on landlord responsibilities to passive multifamily syndication.

If you’re fatigued by active management, consider passive investing in institutional-quality apartment complexes. Some of the benefits include:

Are you tired of fixing leaky toilets, hiring contractors for roof replacement, or dealing with the stress of unexpected vacancies? You can say goodbye to those pain points when you partner with a general real estate partner.

BAM Capital handles the heavy lifting—from acquisition and refinancing to leasing and maintenance—which allows investors to move into a passive role while remaining subject to the risks associated with third-party management.

While single-family rentals focus on small monthly checks, a growth-focused multifamily fund prioritizes long-term appreciation and equity build-up. By applying institutional-grade management to increase the property’s value, the objective is to help investors significantly grow their capital over a typical 3- to 7-year hold period, during which the asset is optimized for sale.

At BAM Capital, our investment strategy aims for a 15-20% net internal rate of return (IRR) and an equity multiple of 2.0-2.5x. To put that in perspective, a $200,000 investment is targeted to more than double by the time the fund’s hold period ends, although this is a projection and actual results may vary based on market conditions and fund performance.

Multifamily assets generally offer a degree of stability compared to more volatile markets, though like all real estate investments, they carry inherent risks of vacancy and income fluctuation. If one unit is vacant, others still generate income.

As a vertically integrated real estate sponsor, BAM Capital prioritizes improving properties and optimizing operations to increase net operating income (NOI) and property value. This may include physical upgrades like installing stainless steel appliances or adding tech-friendly features such as smart locks. It can also involve operational improvements such as optimizing rents, reducing vacancies, negotiating vendor contracts, and increasing ancillary income, which can translate directly into forced appreciation.

Real estate is a rare investment where the IRS allows you to grow wealth through accelerated depreciation, potentially giving you the ability to offset passive income with passive losses, subject to IRS limitations.

Start with a critical review of your portfolio’s performance and capital needs. Identify which assets are worth holding and where equity is tied up, then redirect it toward more efficient, passive opportunities.

Most multifamily real estate investment opportunities are for accredited investors, which is defined by the SEC, but generally means having a net worth of $1 million (excluding a primary residence) or earning $200,000 in each of the two most recent years ($300,000 for couples), with a reasonable expectation of maintaining that income level.

Schedule a call with the BAM Capital investor relations team to discuss goals, risk factors, and align on investment strategies. Examine the Private Placement Memorandum (PPM), financial projections, and detailed business plans for the specific multifamily fund.

Review available offerings, including business plans, projected returns, and hold periods. If you find an investment that fits your needs, you complete the subscription process and fund the deal while the BAM Capital team handles acquisition and execution. This transitions you from concentrated, hands-on ownership to diversified, professionally managed assets.

In this role, you trade high-maintenance property management for an institutionally managed, diversified portfolio. Instead of fielding tenant complaints, you simply review performance updates. The potential for income and long-term growth remains, but the weight of daily operations is permanently lifted from your shoulders.

Stepping away from landlording can feel like a big decision. Your properties represent time, effort, and capital, but the ongoing demands can start to outweigh the returns. If you’re ready for a change, passive multifamily real estate syndication offers a way to keep your money working without the burden of active management.

BAM Capital has grown into a leader in the private equity real estate space, focusing on institutional-quality apartment communities across the Midwest. With a vertically integrated approach and proven execution, we provide investors with access to scalable, professionally managed assets that are projected to build long-term income and growth.

Book a call today to connect with our team.

Disclaimer: This content is for informational purposes only and is not financial, tax, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital and its affiliates are made pursuant to Rule 506(c) of Regulation D, available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers, as defined by Section 2(a)(51) of the Investment Company Act of 1940. Verification of accredited investor status is required before participation in any investment.

Contact BAM Capital for details on current offerings. BAM Capital and its representatives are not fiduciaries or investment advisors. The information provided is general and may not reflect individual financial goals. Financial terms, projections, or forward-looking statements contained herein are hypothetical and should not be interpreted as guarantees of future performance or safety. Such statements reflect BAM Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including, without limitation, illiquidity, economic downturns, and potential loss of invested funds or capital. Past performance does not predict or guarantee future results. Historical transaction figures represent past performance across multiple deals as of the date this information was published, not a single investment transaction. BAM Capital and its affiliates do not guarantee the accuracy or completeness of this information. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2026 BAM Capital. All rights reserved.

Dear Fund IV Investors,

I’m writing to share my perspective and insight on BAM Multifamily Growth & Income Fund IV — where it stands today, where I believe it is headed, and why my conviction in this portfolio is stronger than current performance marks might suggest.

Fund IV is a recent-vintage fund comprising six communities assembled between May 2023 and August 2024. The timing places us directly into the teeth of the sharpest interest rate cycle in forty years. Rent growth across the portfolio has been essentially flat since inception, up just 0.3% and B Share preferred returns continue to accrue. I won’t gloss over those facts.

But that is the paper. Here is what is actually happening underneath it and why I am excited about these assets.

The assets are good, and they are performing. Fund IV is 1,626 units across six Class A communities — in Noblesville, Fishers, and Whitestown, Indiana; Rogers, Arkansas; Wexford, Pennsylvania; and Kansas City, Missouri. These are newer properties in supply-constrained, growth-oriented submarkets, the kind of real estate that is very difficult to build today at a price that pencils. Net operating income is up 6.5% since inception and, in the first quarter, came in ahead of budget at $4.35 million. Portfolio occupancy has climbed to 90.8%, up 240 basis points from a year ago, and collections are running at 98.1%. These are not the numbers of a portfolio in trouble. They are the numbers of a portfolio grinding its way up.

Several assets are already showing what this fund can do. Altitude 970 in North Kansas City reached 94.8% occupancy this quarter, its highest since we acquired it, with trailing NOI up 16.3% year over year. Ascent 430 outside Pittsburgh grew NOI 27.4% year over year as occupancy recovered from 85% to nearly 89%. This is exactly the operational alpha we built BAM to capture, and it is starting to come through. Nese, in Whitestown, Indiana, points to the kind of demand tailwind building ahead of this fund: occupancy climbed to 91.6% in the first quarter, well ahead of plan, and the property sits in Boone County — home to the LEAP Research and Innovation District in neighboring Lebanon. Eli Lilly has now committed more than $20 billion to its Indiana manufacturing build-out anchored there, including what will become the largest active pharmaceutical ingredient plant in the country, and that wave of high-wage jobs is only beginning to translate into rental demand on Nese’s doorstep.

We are taking cost out of the portfolio. In the fourth quarter we moved all six assets onto a single master insurance policy, cutting average per-unit insurance cost from roughly $750 to $520 a year. In a period when insurance has punished multifamily owners across the country, we pushed ours down, and that savings flows straight to NOI for the rest of 2026 and beyond. We are actively managing the capital structure to navigate this macro environment. Fund IV currently carries a 66.4% loan-to-value and a debt service coverage ratio of 1.21x. While these metrics represent an improvement over last quarter, we recognize that the current economic environment requires a disciplined, defensive posture. To that end, we currently have $12.5 million in reserves to provide the runway that ensures the A Share preferred investors continue to receive their 10% annualized distribution, paid monthly. Our focus is on operational execution; we have the liquidity to manage through the current cash flow constraints and are under no pressure to execute forced asset sales at the bottom of the cycle.

Now, here is why I’m genuinely excited.

Fund IV’s value looks muted because of the denominator and the timing, not the real estate. Interest rates have stayed higher for longer than almost anyone expected, and cap rates have stayed elevated right alongside them. At the same time, we haven’t yet seen income growth bounce back, because the wave of new supply delivered over the past few years still needs to burn off before rents can reaccelerate. The result is that the same dollar of NOI is capitalized at a lower value than it would have commanded three years ago, which has compressed values for every multifamily owner in America, ours included. But it is a math problem that reverses. We own newer Class A product at a basis at least 15% below current replacement cost — we could not build these communities today for what we paid for them — in markets where very little new supply is coming behind us. Construction starts have collapsed from their 2022 peak, and the delivery pipeline falls off a cliff in 2028 and beyond. As that excess supply is absorbed and debt markets normalize, income growth returns and cap rates compress, and the value of this same portfolio moves meaningfully in the other direction. We do not need a heroic outcome here; we need the cycle to do what cycles do.

I have been buying multifamily in these markets for sixteen years, and I’ll tell you plainly: owning newer Class A communities at this basis, with this little new supply coming behind them, is not how this product normally trades. We got into Fund IV at prices the next cycle will not offer again. That is why I look at the interim marks with patience rather than worry, and why I believe that when we look back at this fund in five years, the basis we established in 2023 and 2024 will be the headline of the story, not the marks we are carrying today.

Thank you for your trust and for your patience. The hardest part of a cycle is also where the best deals are made, and I am convinced Fund IV will prove to be a strong vintage. As always, my door is open. I’m glad to walk through any asset or answer any question, and our capital markets and investor relations team are here whenever you need them.

With gratitude,

Ivan Barratt

Founder & CEO

The BAM Companies

This communication is for existing investors in BAM Multifamily Growth & Income Fund IV and is not an offer to buy or sell securities. It does not constitute financial, legal, or investment advice. Performance metrics, including the 6.5% NOI growth, are current as of March 31, 2026, and are not indicative of future results. Forward-looking statements regarding market cycles and asset values are estimates and projections based on reasonable assumptions, not guarantees; actual results may differ materially. Private real estate investments involve significant risks, including illiquidity.

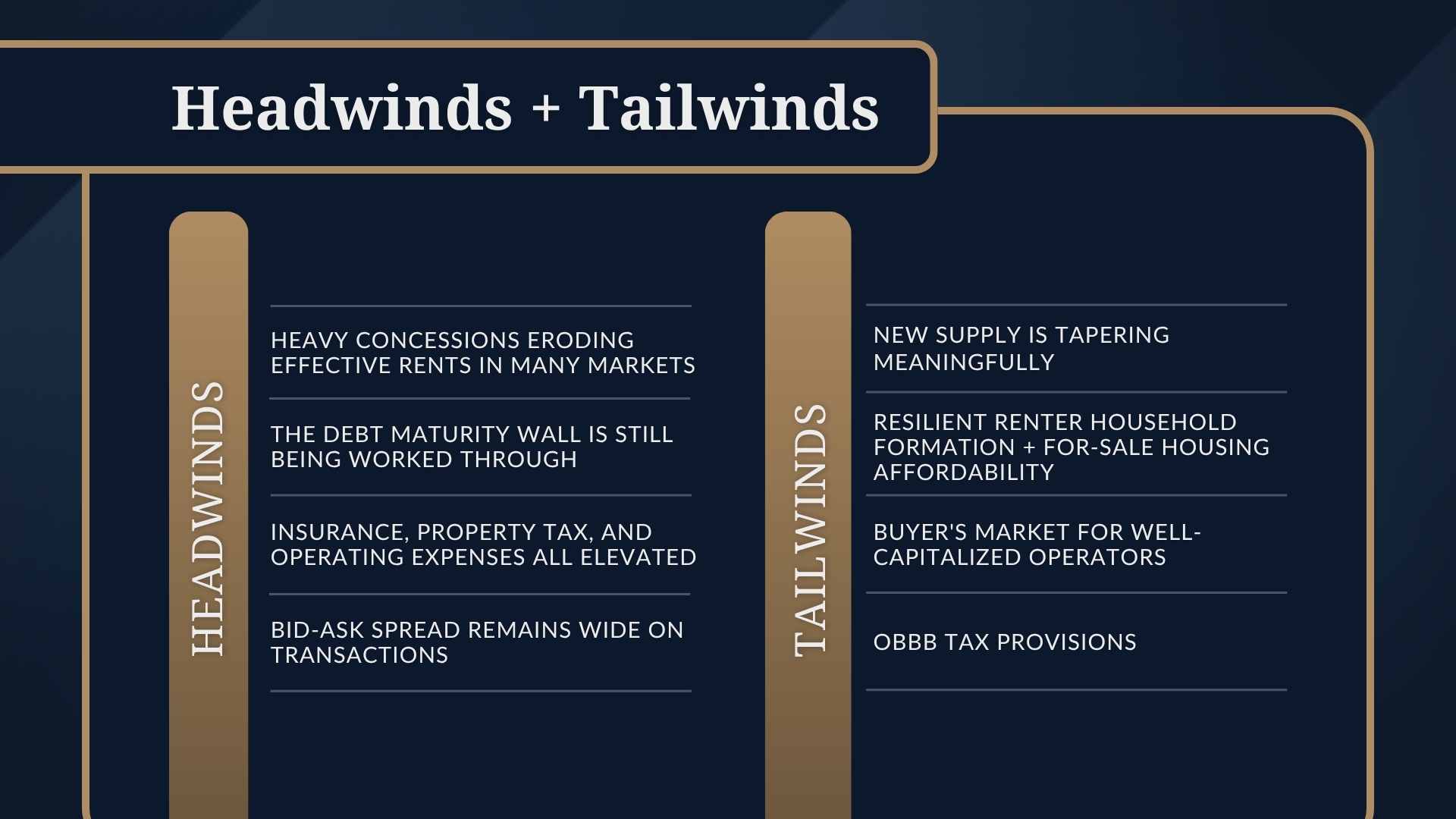

Higher interest rates have made today’s multifamily market one of the most challenging in recent years. But for well-capitalized buyers, this environment also creates opportunity. In our 2026 Founders’ Town Hall, Ivan Barratt and Adam Ehret unpacked these capital market shifts and shared how experienced multifamily investors can successfully navigate the current cycle.

One of the biggest hurdles today is an oversupply of new apartments in certain markets, leading many operators to offer concessions and incentives to attract renters.

Nationally, rent growth has remained relatively flat year over year, reflecting just how competitive leasing conditions have become across much of the country.

The Midwest, where BAM Capital’s portfolio is concentrated, continues to stand out. Data shared during the presentation showed Midwest multifamily markets posting 2.5% year-over-year rent growth, along with stronger occupancy rates and less new supply coming online.

Year-over-year rent growth

Occupancy

Percentage of inventory under construction

Another major challenge across the industry is the “debt maturity wall,” Ivan explained.

Many apartment owners who purchased properties when interest rates were low are now facing loan maturities in today’s higher-rate environment. For some, refinancing has become difficult, especially without bringing in additional capital.

As a result, we’re seeing a trickle of assets come to market, where owners are being forced to sell for one reason or another. “Essentially, anyone that can be patient and wait to sell is waiting,” Ivan told the group.

Because of this, transaction activity remains relatively slow, with buyers and sellers still far apart on pricing in many markets.

Meanwhile, insurance costs, property taxes, and day-to-day operating expenses remain elevated, continuing to pressure property performance.

“We’re still in this buyer’s market,” Ivan said. “It is a fairly good time to buy assets, and we may even see more of a buyer’s market before conditions shift back toward sellers.”

Even with those headwinds, several important trends are beginning to shift in favor of long-term multifamily investors. One of the most notable is the slowdown in new apartment construction.

Ivan explained that development pipelines in some areas are shrinking as higher borrowing costs and lower projected returns make it more difficult to move new projects forward.

“New supply has definitely tapered off meaningfully and has literally fallen off a cliff in some markets,” he said. “Even though there are still lots of units that need to be rented, we’re not seeing additional projects entering the pipeline.”

Demand for rental housing, however, remains strong. The gap between renting and the cost of homeownership continues to widen across many parts of the country. Higher mortgage rates and home prices have pushed homeownership further out of reach for many households, keeping more people in the rental market for longer.

That combination of limited new supply and steady renter demand is creating more favorable long-term conditions for multifamily investors.

It was also noted that pricing on some acquisitions is beginning to approach replacement cost, with select assets trading near what it would cost to build new today.

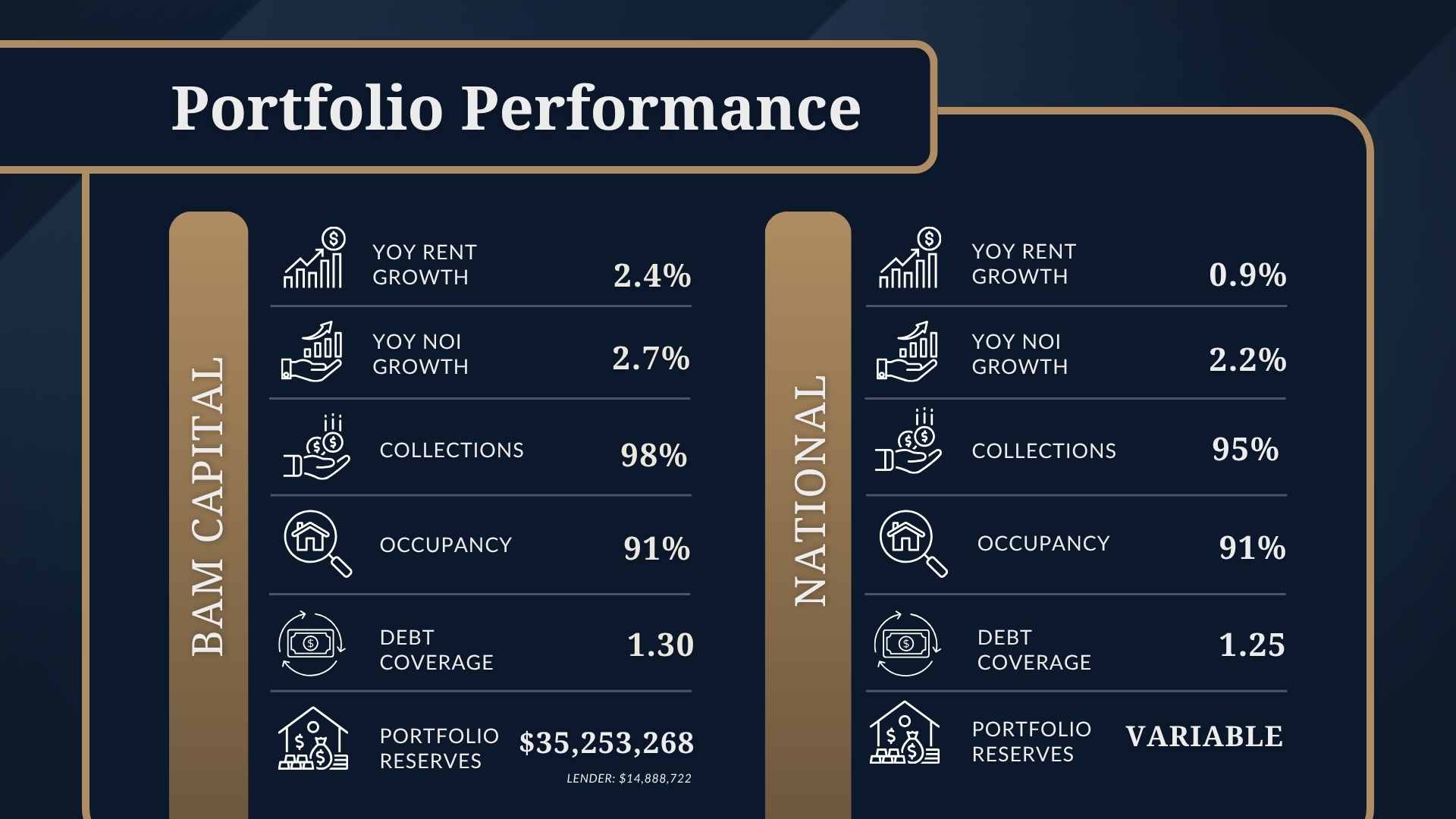

The team shared that occupancy and NOI growth are not currently where they would like them to be given today’s market conditions. Even so, BAM Capital’s portfolio continues to outperform many national benchmarks across several key metrics.

Over the firm’s track record, BAM Capital has generated a 32.19% net IRR and a 2.36x equity multiple, reflecting a long-term focus on disciplined acquisitions and operational execution across different market cycles.

BAM Capital prioritized keeping strong cash reserves, which helps us meet lender requirements and protects the portfolio from market volatility. Early signs suggest that some capital may gradually begin flowing back into the market as investors position for the next phase of the cycle.

The market is still adjusting, but the team believes patient, well-capitalized buyers may be positioned to benefit as conditions continue to evolve.

For many high-income earners, stock market ups and downs can feel unpredictable and difficult to control. That’s why many investors are turning to multifamily real estate for the potential of greater stability, consistent income, and long-term growth.

The good news is you don’t need to manage properties yourself or have millions in cash to get started. With firms like BAM Capital, passive investing in apartment complexes has opened the door to institutional-quality multifamily real estate without the day-to-day responsibilities.

When learning how to invest in apartment buildings, the first decision is determining whether you want a second job or a passive investment.

The active route often means sourcing deals, managing tenants, overseeing renovations, and handling operations. While it offers more control, it also requires time and expertise and exposes you to higher risk if a property underperforms.

Passive investing, BAM Capital’s core focus, looks very different. You invest as a limited partner while an experienced team — referred to as a general partner — handles acquisitions, financing, property management, and execution through a vertically integrated platform, a model that sets BAM apart from most real estate sponsors. Instead of owning and managing single-family rental homes, you gain exposure to large, professionally managed Class A apartment communities.

For many busy professionals, this approach makes more sense because it allows you to diversify and invest in thousands of units without sacrificing your time. Firms like BAM Capital make this possible through a proven track record, including over $1.85B in historical transaction volume across a portfolio of more than 10,000 units.

Private equity investments in apartment communities excel historically because they combine income, scalability, and sustained capital appreciation in one asset class.

Are you tired of fixing leaky toilets or replacing broken air conditioners? One of the most attractive benefits of passive investing in apartment complexes is avoiding landlord responsibilities. With BAM Capital’s vertically integrated team, everything from leasing to maintenance is handled for you, providing a truly hands-off experience.

Having a sponsor manage 200 units under one roof is far more efficient than owning and operating 200 (or even 10) single-family homes scattered across different locations. Partnering with a general partner like BAM Capital has the potential to reduce overhead, streamline operations, and facilitate growth through economies of scale.

Investors may benefit from powerful tax advantages that significantly improve after-tax returns. Strategies like depreciation and cost segregation can help offset passive income.

Apartment buildings generate consistent income through rent payments. With multiple tenants, the risk of vacancy is spread out, creating the potential for more stable and predictable cash flow. The historical performance of BAM Capital’s multifamily syndications has resulted in a historical average Net IRR of 32.19%, representing the total annualized return to investors based on all cash flows over time. However, like all private real estate, these investments involve risks, including the potential loss of capital.

Rental housing continues to see strong, sustained demand as a fundamental need, particularly in stable Midwest markets. This combination of high-demand housing and market stability drives long-term performance.

Unlike single-family homes, multifamily communities offer the opportunity for forced appreciation. By streamlining operations, optimizing rents, or reducing overhead, an operator can manually drive the property’s value higher. This shifts the investment’s success into the hands of the operator, providing a hedge against stagnant market conditions.

Investors also benefit from economies of scale, professional management, and access to opportunities that would otherwise be out of reach. Together, these factors make multifamily apartment investing a compelling strategy.

Before investing in apartment buildings, it’s important to understand how returns are measured in multifamily deals.

Entering the world of passive multifamily apartment investing is more straightforward than most accredited investors expect, especially when you partner with an experienced private equity firm such as BAM Capital.

Once qualified, you can review our current offerings. Investors can access BAM Capital’s multifamily funds targeting risk-adjusted returns, including current offerings with a projected 15-20% net IRR. Please note these projections are hypothetical and actual results may materially differ.

BAM Capital’s investment opportunities are available to accredited investors, typically defined as having a net worth over $1 million (excluding a primary residence) or earning $200,000 in each of the two most recent years ($300,000 for couples).

After choosing an investment, you’ll complete documentation, such as a Subscription Agreement, after reviewing the Private Placement Memorandum (PPM). The PPM acts as a vital disclosure document, detailing the risk factors and the equity waterfall structure. From there, the BAM Capital team handles execution, and investors begin receiving updates and distributions based on the deal structure.

BAM Capital has positioned itself as a top-tier owner-operator of institutional-quality apartment communities across the Midwest. Our approach focuses on balancing consistent cash flow, capital preservation, and long-term appreciation.

With over $248 million in total distributions and a disciplined investment strategy centered on forced appreciation, our firm has built a track record that appeals to investors seeking both growth and stability.

Our vertically integrated model also differentiates us. Instead of outsourcing key operations, we maintain control over acquisitions, management, and execution to help ensure alignment between the investment strategy and performance.

Apartment investing has evolved. What was once limited to large institutions is now accessible to individual investors through passive private equity models.

At its core, passive multifamily syndication is designed to generate consistent cash flow while simultaneously growing long-term wealth. By partnering with an experienced sponsor, you secure the financial rewards of high-quality assets without the operational burdens of active management.

If you’re exploring ways to diversify beyond stocks and create more predictable income, passive multifamily investing is worth a closer look. Ready to learn more? Schedule a discovery call with the BAM Capital team to explore current opportunities and see if this strategy aligns with your financial goals.

Disclaimer: This content is for informational purposes only and is not financial, tax, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital and its affiliates are made pursuant to Rule 506(c) of Regulation D, available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers, as defined by Section 2(a)(51) of the Investment Company Act of 1940. Verification of accredited investor status is required before participation in any investment.

Contact BAM Capital for details on current offerings. BAM Capital and its representatives are not fiduciaries or investment advisors. The information provided is general and may not reflect individual financial goals. Financial terms, projections, or forward-looking statements contained herein are hypothetical and should not be interpreted as guarantees of future performance or safety. Such statements reflect BAM Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including, without limitation, illiquidity, economic downturns, and potential loss of invested funds or capital. Past performance does not predict or guarantee future results. Historical transaction figures represent past performance across multiple deals as of the date this information was published, not a single investment transaction. BAM Capital and its affiliates do not guarantee the accuracy or completeness of this information. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2026 BAM Capital. All rights reserved.

The BAM Companies' annual BAMily Reunion | Recap | 2026

Q1 2026 Event | The BAM Companies

The BAM Companies 2025 Year in Review: 15 Years of Growth and Excellence

The BAM Companies Christmas Gala & Awards Ceremony 2025

BAMcon 2025 | Our All-Company Conference

Our President's "why" | A message from Adam Ehret

Our secret to success? We put our employees first.

On-Site Day 2025 | The BAM Companies

2025 The BAM Companies Q1 All Company Event - The Fowling Warehouse

One word about The BAM Companies

The BAM Companies Christmas Party & Annual Awards Ceremony 2024

BAMcon 2024 | The BAM Companies' annual all-company event

History doesn’t repeat itself, but it rhymes — and right now it’s rhyming loudly with the mid-to-late 1940s. In 1946, the United States emerged from World War II with federal debt at 106% of GDP, the highest in its history. This year, for the first time since that era, debt held by the public crossed 100% of GDP again, and the Congressional Budget Office projects it will reach 120% within a decade. Layer on political fracture and income inequality at levels last seen around the war years, and the parallel becomes hard to ignore.

The question that matters for investors isn’t whether Washington will deal with this debt. It’s how. And the last time America faced this exact problem, the answer wasn’t austerity, default, or a miracle of growth. It was the Federal Reserve — quietly, deliberately, and at the expense of anyone holding bonds and cash.

Debt. The 1946 peak of 106% came from a war that had ended; the bills stopped arriving. Today’s 100% comes with peacetime deficits running north of 6% of GDP and entitlement spending that compounds on autopilot. In one sense, our position is more challenging than 1946 — the borrowing hasn’t stopped.

Division. We tend to remember the late 1940s through a sepia filter of unity, but Americans living through it experienced something closer to chaos. In 1946, roughly five million workers walked off the job in the largest strike wave in U.S. history. Inflation hit double digits as price controls came off. Truman waged open war with what he called the “Do-Nothing Congress,” and the first loyalty scares that became McCarthyism were already brewing. Distrust in institutions, anger over the cost of living, fights between labor and capital — it all sounds familiar.

Inequality. Before the war, the top 1% of Americans earned more than 20% of national income. The 1940s produced what economists call the Great Compression — a dramatic flattening driven by wartime wage controls, confiscatory top tax rates, surging union membership, and inflation that quietly devalued old fortunes. Today, the top 1% share has round-tripped back above 20%, union membership has fallen from over 30% of the workforce to roughly 10%, and the political pressure that builds in such conditions is visible everywhere.

From 1942 to 1951, the Federal Reserve didn’t set interest rates the way we think of today — it pegged them. Treasury bills were capped at 0.375% and the long bond at 2.5%, and the Fed bought whatever quantity of government debt was necessary to hold those ceilings. Call it what it was: debt monetization in service of the Treasury. The central bank was, for nearly a decade, an arm of war finance.

Then came the crucial part. When price controls lifted in 1946, inflation surged — 8% in 1946, north of 14% in 1947 — while the Fed held nominal rates pinned near zero on the short end. Real interest rates went deeply negative. Every saver holding a Treasury bond or a bank deposit earned a yield far below inflation, year after year. Economists call this financial repression. It is a wealth transfer from lenders to borrowers, and the borrower-in-chief was the U.S. government.

It worked. Debt-to-GDP fell from 106% in 1946 to 23% by 1974. The comfortable story is that America “grew its way out.” The data says otherwise: recent IMF and NBER research decomposing that decline finds that growth alone would have taken the ratio only from 106% to about 74%. The majority of the heavy lifting came from primary surpluses, surprise inflation, and interest-rate distortion — the Fed holding rates below inflation. Bondholders paid down the war debt without ever receiving a default notice. The arrangement lasted until the Treasury-Fed Accord of March 1951 restored the Fed’s independence — but only after the repression had done its work.

The 1940s analog isn’t just monetary — it’s industrial. Postwar America converted its war machine into the world’s dominant manufacturing base, and when Washington wanted to build at scale, it reached for the language of national security. The 1956 highway bill that built the interstate system was formally titled the National Interstate and Defense Highways Act. Defense was the political wrapper around a generational infrastructure buildout.

That template is back. The FY2027 defense request of roughly $1.5 trillion — on top of a record $1 trillion for FY2026 — represents the largest defense ramp since the Korean War, with massive line items for shipbuilding, munitions production, and the “Golden Dome” missile defense program. The CHIPS Act has catalyzed more than $630 billion of announced semiconductor investment across 140 projects. Real manufacturing construction spending has more than doubled since 2021. The Pentagon is directly funding rare-earth magnet plants and lithium mines to rebuild domestic supply chains. Reshoring initiatives tracked roughly a quarter-million announced manufacturing jobs in 2024 alone.

Strip away the program names and you have the 1940s formula: government-directed capital flooding into factories, energy, logistics, and defense infrastructure — spending that is structural, politically durable because it wears a national-security badge, and inherently inflationary because it consumes real resources, labor, and materials.

Here is the uncomfortable arithmetic: net interest on the federal debt now rivals the defense budget itself. At today’s debt levels, every percentage point of interest rates costs the Treasury hundreds of billions per year. No Congress of either party will run the multi-trillion-dollar surpluses needed to pay debt down honestly, and outright default is unthinkable. That leaves one historically proven exit — the 1940s one: hold nominal rates below inflation and let the debt melt in real terms.

I don’t expect the Fed to announce formal yield curve control with a press release. I expect it by increments, and the increments have arguably begun. Quantitative tightening ended in December 2025, and the Fed is again buying roughly $40 billion of Treasury bills per month — framed as “reserve management,” but mechanically indistinguishable from monetizing a portion of new issuance. A new Fed chair has taken office under a president openly demanding lower rates. Bank regulation is being reshaped in ways that encourage institutions to hold more Treasuries. The Treasury itself is leaning on short-dated issuance the Fed can most easily absorb. Each step is defensible in isolation; together they trace the outline of fiscal dominance — monetary policy gradually subordinated to the government’s financing needs, exactly as it was from 1942 to 1951.

The likely end state: inflation that runs persistently in the 3–4% range while policy rates and long yields are managed below where free markets would set them. Not hyperinflation — the 1940s never saw that either. Just a decade or more of quietly negative real rates doing silent, compounding work on the debt ratio. The savers of the late 1940s never got a vote, and neither will today’s.

Financial repression is a transfer from lenders to borrowers. Position yourself on the right side of that transfer.

The designated losers are long-dated nominal bonds and cash. From the mid-1940s through the bond bear market that followed, Treasury holders lost more than half their purchasing power in real terms — the era that earned bonds the nickname “certificates of confiscation.” If the playbook repeats, the 60/40 portfolio’s ballast becomes its anchor.

The winners are productive hard assets whose income rises with inflation — and especially those that can be financed with long-term, fixed-rate debt. Income-producing real estate is doubly advantaged in this regime: rents and replacement costs ride inflation upward while the real value of the mortgage erodes — the investor becomes a beneficiary of the same repression that punishes the bondholder. Housing in particular sits at the intersection of inflation protection and a structural national shortage. Beyond real estate, the reindustrialization wave creates a tailwind for industrial property, energy, infrastructure, and the communities surrounding reshoring corridors, where hundreds of billions in factory investment translate into jobs, wages, and housing demand.

The honest caveats: history rhymes, it doesn’t repeat. An AI-driven productivity boom could lift growth enough to soften the arithmetic, or a genuine austerity turn in Washington could change the path. And none of this is investment advice — it’s a framework. But when I look at debt at World War II levels, a Fed balance sheet growing again, the largest defense buildup since Korea, and factories rising across the heartland for the first time in two generations, I see 1946 — and I’d rather own the assets that era rewarded than the paper it quietly confiscated.

Ivan Barratt

Founder & CEO

The BAM Companies

This article reflects the author’s opinions and is provided for informational purposes only; it does not constitute investment, legal, or tax advice.

Syndications and funds are often used interchangeably in multifamily real estate, but they are structured differently and offer distinct experiences for investors, even though both provide access to the asset class.

In a traditional syndication, investors typically place capital into a single, specific property. That means you can review the individual asset, the market, and the business plan before deciding whether to invest.

A fund works differently: your capital is pooled and allocated across multiple investments selected by the sponsor. While this involves risks related to the sponsor’s discretion and fund-level administrative expenses, a fund can also leverage economies of scale—such as consolidated legal, accounting, and operational costs—spread across a broader portfolio.

The difference often comes down to what matters most to you.

A syndication can offer:

A fund can offer:

With a fund, you may not need to evaluate every deal yourself, but that also means placing more trust in the sponsor making those decisions for you.

That is why experience, discipline, and operational quality matter even more in a fund structure.

For investors who want passive exposure without reviewing every opportunity individually, a fund can provide a simpler way to invest.

If you would like to see how BAM Capital’s fund structure works, request access to the Fund Offering Memorandum to review the strategy in more detail.

Disclaimer: This content is for informational purposes only and is not financial, tax, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital and its affiliates are made pursuant to Rule 506(c) of Regulation D, available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers, as defined by Section 2(a)(51) of the Investment Company Act of 1940. Verification of accredited investor status is required before participation in any investment.

Contact BAM Capital for details on current offerings. BAM Capital and its representatives are not fiduciaries or investment advisors. The information provided is general and may not reflect individual financial goals. Financial terms, projections, or forward-looking statements contained herein are hypothetical and should not be interpreted as guarantees of future performance or safety. Such statements reflect BAM Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including, without limitation, illiquidity, economic downturns, and potential loss of invested funds or capital. Past performance does not predict or guarantee future results. Historical transaction figures represent past performance across multiple deals as of the date this information was published, not a single investment transaction. BAM Capital and its affiliates do not guarantee the accuracy or completeness of this information. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2026 BAM Capital. All rights reserved.

One of the reasons some investors hesitate before making their first passive real estate investment is uncertainty about what to expect at tax time.

They have heard about K-1s, depreciation, and paper losses, but the reporting can feel unfamiliar at first.

The good news is that a K-1 is usually much simpler than it seems once you understand what it is showing.

When you invest in a private real estate fund as a limited partner, you are typically investing through a partnership structure, which means you receive an IRS Schedule K-1 instead of a 1099. This form is generated from the partnership’s annual tax return (Form 1065) and reports your share of the entity’s income, deductions, and credits for the year.

Your CPA or tax professional will use the information on your Schedule K-1 to prepare your personal tax return. You don’t need to file the K-1 separately. Instead, the form reports your share of the multifamily property’s income, depreciation-related deductions, losses, and other tax items, which are incorporated into your individual tax return.

Every K-1 can look a little different, but a few sections usually matter most to investors:

For many investors, the most surprising part is that a property can generate cash distributions while still showing a taxable loss on paper because of depreciation.

Real estate allows investors to depreciate the value of the property over time. Those depreciation deductions often flow through the K-1 and can help offset passive income from other real estate investments.

That means your K-1 can also give you a clearer picture of how your investment is performing behind the scenes.

K-1s are typically issued after year-end once the partnership’s reporting is complete. At BAM Capital, our team works to provide investor reporting as clearly as possible so you understand what you are receiving and when to expect it.

For many investors, the first K-1 feels unfamiliar. After that, it often becomes one of the most useful documents they receive all year.

If you’d like to better understand how tax reporting works within a private real estate fund, reach out to the BAM Capital investor relations team at invest@bamcapital.com to discuss your questions and learn how it may apply to your investment strategy.

Disclaimer: This content is for informational purposes only and is not financial, tax, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital and its affiliates are made pursuant to Rule 506(c) of Regulation D, available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers, as defined by Section 2(a)(51) of the Investment Company Act of 1940. Verification of accredited investor status is required before participation in any investment.

Contact BAM Capital for details on current offerings. BAM Capital and its representatives are not fiduciaries or investment advisors. The information provided is general and may not reflect individual financial goals. Financial terms, projections, or forward-looking statements contained herein are hypothetical and should not be interpreted as guarantees of future performance or safety. Such statements reflect BAM Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including, without limitation, illiquidity, economic downturns, and potential loss of invested funds or capital. Past performance does not predict or guarantee future results. Historical transaction figures represent past performance across multiple deals as of the date this information was published, not a single investment transaction. BAM Capital and its affiliates do not guarantee the accuracy or completeness of this information. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2026 BAM Capital. All rights reserved.

The BAM Companies is proud to announce that it has earned the prestigious 2026 USA TODAY Top Workplaces award. The BAM Companies also received this award in 2023, 2024, and 2025.

The award honors organizations with 150 or more employees that have created exceptional, people-first cultures. This year, more than 40,500 organizations were invited to participate. The winners are recognized for their commitment to fostering a workplace environment that values employee listening and engagement. USA TODAY showcased the winners online and at the National Awards Summit in Nashville.

Additionally, The BAM Companies was named to USA TODAY’s Purpose & Values Top Workplaces, Compensation & Benefits Top Workplaces, Work-Life Flexibility Top Workplaces, Leadership Top Workplaces, Innovation Top Workplaces, Employee Well-Being Top Workplaces, Top Workplaces for Appreciation, Professional Development Top Workplaces, and Real Estate Top Workplaces.

"A company is only as good as its people,” said Emilee Meyers, The BAM Companies COO. “You can have a great strategy, a great product, and great ideas, but none of it matters without great people behind it. What makes me most proud isn’t the award itself—it’s that we’ve built a place where talented people want to show up, contribute, grow, and do meaningful work together. We don’t take recognition like this from USA TODAY for granted. Every person on this team had a hand in earning it. And maybe I’m biased, but I’d take this team over any other. Every day of the week. The best things we’ve accomplished are a direct result of the people who make The BAM Companies what it is, and the future is exciting because they’re the ones helping build it.”

The winners are determined by authentic employee feedback captured through a confidential survey conducted by Energage, the HR research and technology company behind the Top Workplaces program since 2006. The results are calculated based on employee responses to statements about Workplace Experience Themes, which are proven indicators of high performance.

“Earning a USA TODAY Top Workplaces award is a testament to an organization’s credibility and commitment to a people-first culture," said Eric Rubino, CEO of Energage. "This award, driven by real employee feedback, is more than just a recognition — it’s proof that your employees believe in the organization and its leadership. Job seekers and customers look for this trusted badge of credibility and excellence. It signals a company that values its people, and that kind of culture resonates in today’s competitive market”

About The BAM Companies

Headquartered in Carmel, Indiana, The BAM Companies specializes in the acquisition and management of multifamily apartment communities. Comprising BAM Capital, BAM Management, and BAM Construction, The BAM Companies has been named as the Indiana Apartment Association’s 2024 Management Company of the Year, a Top Workplace by IndyStar for four consecutive years, a recipient of the Indianapolis Business Journal’s Fast 25 award, and is one of Inc.’s 5000 fastest-growing private companies in America for the last eight consecutive years.

If you’ve spent any time evaluating real estate investments, you’ve likely encountered two metrics repeatedly: Internal Rate of Return (IRR) and equity multiple.

When weighing equity multiple vs IRR, it’s important to remember that while both measure returns, they tell very different stories about a deal’s performance. Understanding this distinction is essential for evaluating investments with clarity and confidence.

By seeing how IRR and equity multiple (also known as MOIC, or multiple on invested capital) work together, you can set more realistic expectations, make informed decisions, and avoid relying on single numbers that only tell part of the story.

At its core, IRR measures the velocity of your money. While the technical definition is the discount rate that brings the net present value (NPV) of all cash flows to zero, in practical terms, IRR shows the compounded annual rate at which your capital grows over the life of an investment.

Because of the time value of money, a dollar earned in year one is generally more valuable than a dollar earned in year five—and IRR accounts for that by placing greater weight on earlier cash flows.

Beyond timing, IRR incorporates both ongoing income and sale proceeds, expressed as an annualized percentage. Unlike total ROI, which measures overall gain regardless of time, IRR shows how efficiently your capital is working on a yearly basis.

In real estate investing, IRR is typically measured over a multi-year hold—often 3 to 7 years—reflecting the full lifecycle of a deal from acquisition through exit.

It’s important to note that IRR relies on projected cash flows and is highly sensitive to underlying assumptions, meaning its accuracy is only as good as the data behind it. While it reflects the timing of returns, it is most powerful when paired with metrics like the equity multiple to see the full picture of value creation.

Equity multiple measures the total cash returned relative to the amount invested over the life of a deal.

Formula:

Equity Multiple = Total Cash Returned / Total Invested Capital

Examples:

It does not matter whether that return occurs over two years or 10—equity multiple focuses purely on total capital returned. Because of this, a higher multiple over a longer hold period may appear attractive, but it does not account for how long your capital is tied up.

What equity multiple tells you:

Because it does not account for the time value of money, equity multiple is best used alongside IRR to evaluate both total return and timing. This is a key distinction in any MOIC vs IRR comparison.

There is no universal benchmark, as returns depend on strategy, risk profile, and hold period. In multifamily real estate, many investors target IRRs in the mid-teens to low-20 percent range, along with equity multiples between roughly 1.8x and 2.5x.

Some investors may pursue higher IRRs, while others prioritize more stable returns over a longer hold period.

An experienced general sponsor can meaningfully influence a deal’s performance. BAM Capital stands out from many real estate syndications by taking a vertically integrated approach, managing everything in-house from acquisition and legal oversight to operations. This structure helps ensure disciplined execution of the business plan and supports more consistent, risk-adjusted outcomes over time.

Looking at actual performance helps put this into perspective. Across a portfolio of realized multifamily assets from BAM Capital, historical results have averaged a 2.36x Net equity multiple and a 32.19% Net IRR. This consistent track record reflects our commitment to targeting strong returns and efficient timelines, keeping in mind that past success does not guarantee future results and all investments carry a risk of loss.

When evaluating real estate deals, IRR and equity multiple are most powerful when used as complementary tools. While IRR measures the speed of your return, the equity multiple confirms the total wealth created. Understanding how equity multiple vs IRR work together helps investors balance return speed with total wealth creation.

If you’re ready to see how these metrics apply to real-world multifamily opportunities, the investor relations team at BAM Capital can walk you through our current offerings and help you evaluate how they align with your portfolio goals.

Disclaimer: This content is for informational purposes only and is not financial, tax, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital and its affiliates are made pursuant to Rule 506(c) of Regulation D, available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers, as defined by Section 2(a)(51) of the Investment Company Act of 1940. Verification of accredited investor status is required before participation in any investment.