What’s the difference between an in-place capitalization rate, the return on cost, and the stabilized yield? The differences are subtle but invaluable when evaluating real estate opportunities. Not one metric will define a good investment, but it takes a combination of the three to have a comprehensive understanding of real estate valuation and how these metrics are interconnected.

- In-Place Capitalization Rate: An “in-place” or “going-in” capitalization rate (cap rate) is a metric used in real estate valuation that reflects the initial return on investment based on the property’s current net operating income (NOI) relative to the purchase price. It’s premature to understand a property’s annualized return in the first year, particularly during the stabilization period where there is below market rents or under market occupancy.

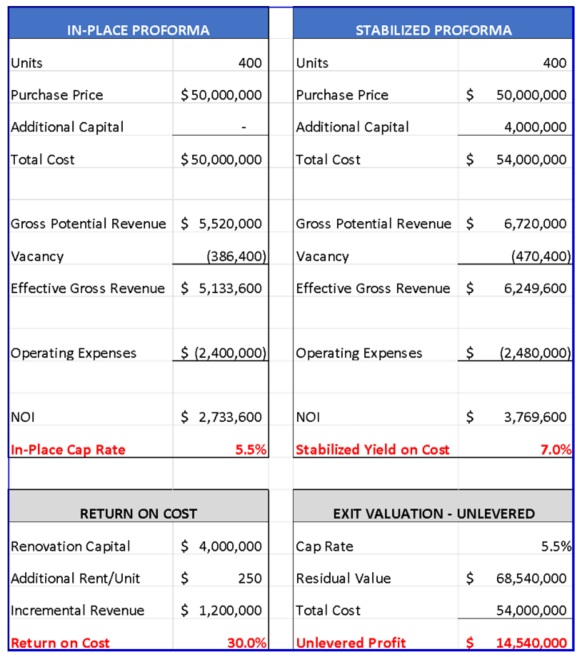

- Return on Cost: When does it make sense to renovate and optimize value? An investor obviously doesn’t invest additional capital in a real estate project unless it’s worth one’s money or exertion. What does that mean? It means looking at math on an unlevered basis and the return percentage on the incremental cash investment. For example, an owner/operator plans to invest another $10,000/unit on a 400-unit apartment community. That’s $4 million of additional capital. However, it will generate a $250/unit premium or $1.2 million in additional revenue, which equates to a 30% return on cost ($1.2 million / $4.0 million). There is no hard and fast rule of thumb to this metric. However, a 20% – 25% is a satisfactory return on cost depending on the original investment basis.

- Stabilized Yield on Cost: This metric is the most important calculation when evaluating a potential real estate opportunity. Real estate is a cash flow business. The trick is to underwrite a property not on in-place cash flow, but on stabilized cash flow as it gives us the intrinsic value of the property.

Let’s connect these three metrics: cap rate, return on cost, and the stabilized yield on cost. An investor acquires an asset for $50 million with an NOI of roughly $2.73 million which equates to a 5.5% in-place cap rate. Subsequent to acquisition, the investor injects another $10,000/unit or $4 million of capital to produce a rent premium of $250/unit or $1.2 million of additional revenue yielding a 30% return on cost. When combined with the initial in-place cap rate of 5.5%, the return on cost of 30% produces a blended stabilized yield of 7.0% This yield is exceptional given the current cap rate environment of 5.0% to 5.5% for quality multifamily assets.

Here is a mathematical illustration of how these financial concepts interconnect and the stabilized yield on cost’s impact on profitability.

Investors should always analyze opportunities on an all-cash without thinking about leverage. If an acquisition opportunity doesn’t work on an all-cash basis, it will never work when applying leverage. These three unlevered metrics (cap rate, return on cost, stabilized yield) will tell us all you need to know about an investment opportunity with the back of an envelope.

HYPOTHETICAL PERFORMANCE DISCLOSURE: THE FINANCIAL CONCEPTS, PROJECTIONS, AND RESULTS PRESENTED (INCLUDING CAP RATE, RETURN ON COST, AND STABILIZED YIELD) ARE PURELY THEORETICAL, FOR ILLUSTRATIVE PURPOSES ONLY, AND ARE NOT BASED ON ACTUAL PERFORMANCE OR RESULTS. ASSUMPTIONS INCLUDE (BUT ARE NOT LIMITED TO) TIMELY DEPLOYMENT OF CAPITAL, ACHIEVEMENT OF PROFORMA RENTS AND OCCUPANCY, AND STABILIZED EXPENSES. ACTUAL RESULTS WILL VARY MATERIALLY AND ARE NOT GUARANTEED. INVESTORS COULD LOSE ALL OR A PORTION OF THEIR INVESTMENT.

Disclaimer: This document is for informational purposes only and is not financial, legal, or investment advice, nor an offer or solicitation to buy or sell securities. Investment opportunities offered by BAM Capital are made pursuant to Rule 506(c) of Regulation D and are available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC). Verification of accredited investor status is required before participation in any investment. The information contained herein reflects the opinions of the author and does not necessarily represent the views of BAM Capital. Any financial terms, projections, or forward-looking statements contained herein are hypothetical in nature and should not be interpreted as guarantees of future performance or safety. Such statements reflect opinions and are subject to market fluctuations, economic conditions, and investment risks. Investing in private real estate securities involves significant risks, including but not limited to illiquidity, economic downturns, and potential loss of invested funds. Past performance does not guarantee future results. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions. The information provided in this article is current as of its publication date, September 2025. BAM Capital makes no representation or warranty regarding the accuracy or completeness of the information contained herein.

© 2026 BAM Capital. All rights reserved.

Author: Tony Landa, Senior Economic Advisor, The BAM Companies, February 2026