In 2025, housing affordability remains stretched. This means continued demand for professionally managed apartment communities with stability, predictability, and services residents can’t get in the for-sale market.

At the same time, the supply of new apartments is tapering off after the peak deliveries of 2024, which means competitive pressure is easing. For investors, these conditions continue to highlight the strength of multifamily real estate funds as a vehicle to capture steady income and long-term appreciation.

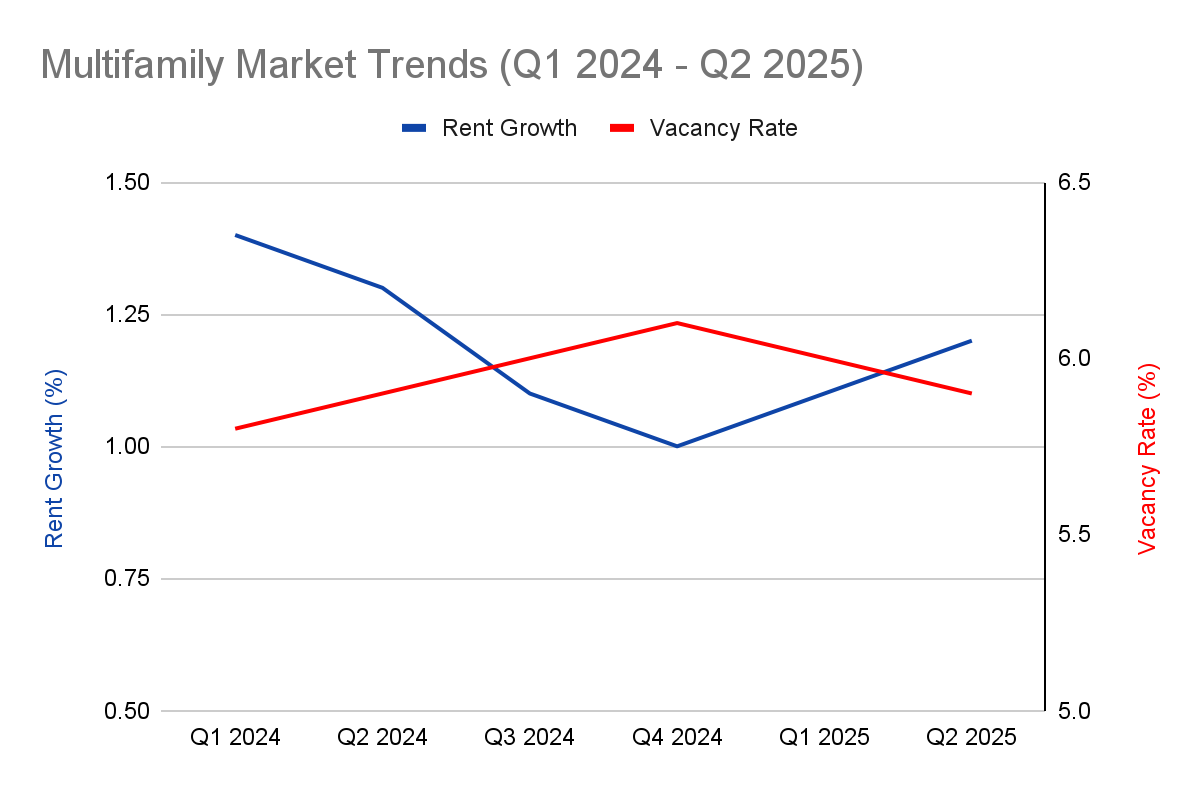

Harvard’s 2025 housing report and the major agency outlooks are all singing the same tune: demand is holding, supply is cooling unevenly, and rent growth is expected to stay positive, even if it is lowering in the near term.

For investors, this is not a bad setup. Steady demand paired with moderating new supply creates a durable floor under multifamily performance. Even if rents don’t spike, they are more likely to grind upward than retrace. That translates into cash flow resilience and more predictable returns.

We’ll cover the implications of this outlook and how it benefits accredited investors, then dig deeper into the most important factors driving multifamily syndication performance below.

Why Multifamily Real Estate Funds Matter in 2025

Multifamily real estate funds offer accredited investors a practical vehicle to tap into the steady demand of rental housing without needing to figure out how to amass enough capital for an apartment community.

While you can own a duplex across town, you may be better off getting a slice of a professionally managed fund. Here’s why:

- Institutional access. Funds pool capital to buy and operate assets commonly valued in the $10M–$400M+ range, properties far beyond most single-investor check sizes. That’s squarely the domain of institutional buyers and ODCE-style core funds.

- Passive by design. The sponsor handles acquisitions, asset management, financing, and exits. You evaluate the manager and the mandate; they do the blocking and tackling.

- Diversification. One fund position can spread exposure across multiple markets, sub-strategies (stabilized, value-add, development), and business plans. So you’re not tied to one submarket’s fortunes.

- Resilience drivers. Affordability constraints keep many households renting longer, demographics keep the prime renting cohort large, and agencies expect positive rent growth with stable-to-slightly higher vacancy in 2025.

Why Not Buy Buildings Outright?

Direct ownership has four main headwinds that funds are built to solve for investors. Those being:

- High capital requirements for institutional assets (equity checks routinely in the millions).

- Operational complexity (leasing, compliance, unit-turns, CapEx).

- Concentration risk in one asset and one local economy.

- Time commitment that’s like a full-time business.

Potential Benefits for Accredited Investors in Multifamily Funds

This section breaks down what MF funds seek to provide to investors:

- Consistent Passive Income: Many closed-end funds target periodic distributions, often with a stated preferred return. Terms vary, and there are no guarantees. Read the PPM.

- Tax Efficiency: Apartments depreciate on a 27.5-year MACRS schedule; cost-segregation studies may accelerate deductions. Passive allocations generally flow through a K-1 and are subject to the passive activity rules.

- Inflation Hedge: Leases reset, operating expenses can be managed, and well-run multifamily assets tend to absorb some inflation over time. Historically, these factors have allowed well-run multifamily assets to absorb some inflation over time, which may be a consideration for investorsseeking an inflation-dampening asset class.

- Diversification: Spread exposure across multiple units, markets, and fund types.

Fund Structures Available

Below is a comparison of the multifamily real estate funds you’ll see in today’s market with a brief overview of each. It’s worth noting that each structure trades control, strategy, and return profile differently.

Comparison of Multifamily Real Estate Fund Structures | ||||

Vehicle | What It Is | Target Objective | Liquidity | Good Fit When… |

Preferred Equity Fund | Capital senior to common equity, junior to debt; contractual priority over common. | Income first, capped upside; downside cushion above common. | Illiquid; periodic distributions per docs; principal via recap/sale. | You want current pay and protection ahead of common, and you’re fine giving up some upside. |

Debt Fund | Originates or acquires senior/mezz loans to multifamily sponsors. | Current income with lower NAV volatility; interest spread capture. | Illiquid; interest/distributions per docs; return of principal at maturity/repay. | You prefer credit exposure and income over equity swings. |

Hybrid Fund | Mix of common equity, preferred equity, and/or credit. | Balanced total return; smoother cash flows across cycles. | Illiquid; terms vary by sleeve mix. | You want one vehicle to balance income and appreciation without manager-hopping. |

Evergreen (Open-End) Fund | Ongoing subscriptions; periodic redemptions at NAV (subject to gates/queues). | Durable income with lower leverage. | periodic redemptions. | You want steady exposure with some rebalancing flexibility (accepting queues/caps). |

Single-Asset Syndication* | One property, single business plan, private placement. | Concentrated total return; line-of-sight to one asset. | Illiquid; distributions from asset cash flow; exit on sale/refi. | You want line-of-sight control on a single business plan and accept concentration risk. |

Multi-Asset Syndication/Fund* | Handful of properties under one vehicle; vintage-dated. | Diversified total return across a small portfolio. | Illiquid; distributions as assets season/exit. | You want more diversification than a single-asset deal without going fully open-end. |

Multifamily Real Estate Returns

Multifamily real estate funds are typically designed to generate two income streams.

- Ongoing income: Some funds are structured to provide cash flow returns either quarterly or semiannually as distributions, often with a stated preferred return. Others may reinvest operating cash flow during the hold period and return capital only at disposition. Whether income is paid during the hold depends entirely on the specific fund strategy.

- Capital appreciation: Value is built over time through rent growth, operational improvements, and, in some cases, renovations or development. When assets are sold or refinanced, investors share the upside through equity multiple and IRR performance.

Multifamily has historically offered lower volatility and more predictable outcomes than many other investment vehicles. However, it’s important to note that they aren’t typically built for quick wins. Instead, they’re usually structured for durable, risk-adjusted returns that compound steadily and provide balance to a portfolio.

How Funds Compare to Other Vehicles

Within multifamily real estate funds, there are many avenues you can take. When evaluating these options, it’s helpful to see how they stack up against one another. The table below provides a side-by-side snapshot for accredited investors to discern which option may be best for them when deciding to invest in them.

Vehicle | Liquidity | Diversification | Fees/Carry | Who can invest? | Typical Hold |

Sponsor-led Multifamily Fund | Low; periodic distributions; no daily liquidity | Multi-asset, multi-market | Mgmt fee + performance “promote” | Accredited investors | 2-10 years |

Crowdfunding platforms | Varies; single deals illiquid; some REITs have repurchase plans | Often single-asset | Varies; watch platform & issuer fees | Reg CF/A for non-accredited | 2-10 years |

Direct private placement | Illiquid | Concentrated in one asset | Deal-specific | Often accredited only (Reg D) | 3-7 years |

Public REITs | Daily | Broad | Mgmt fee embedded; no carry | Public markets, any investor | Open-ended |

Non-traded REITs | Limited liquidity; repurchase programs can gate | Broad | Higher embedded fees common | Varies based on suitability rules | Open-ended |

Why Multifamily Real Estate Funds Are a Good Choice for 2025

Multifamily real estate funds give accredited investors a straightforward way to participate in the consistent demand for rental housing without needing to personally secure the capital or management expertise required to own an entire apartment community.

While you can own a duplex across town, you may be better off getting a slice of a professionally managed fund. Here’s why:

- Institutional access. Funds pool capital to buy and operate assets commonly valued in the $10M–$400M+ range, properties far beyond most single-investor check sizes. That’s squarely the domain of institutional buyers and ODCE-style core funds.

- Passive by design. The sponsor handles acquisitions, asset management, financing, and exits. You evaluate the manager and the mandate; they do the blocking and tackling.

- Diversification. One fund position can spread exposure across multiple markets, sub-strategies (stabilized, value-add, development), and business plans. So you’re not tied to one submarket’s fortunes.

- Resilience drivers. Affordability constraints keep many households renting longer, demographics keep the prime renting cohort large, and agencies expect positive rent growth with stable-to-slightly higher vacancy in 2025.

Why Not Buy Buildings Outright?

Direct ownership has four main headwinds that funds are built to solve for investors. Those being:

- High capital requirements for institutional assets (equity checks routinely in the millions).

- Operational complexity (leasing, compliance, turns, CapEx).

- Concentration risk in one asset and one local economy.

- Time commitment that’s like a full-time business.

Potential Benefits for Accredited Investors in Multifamily Funds

- Consistent Passive Income: Many closed-end funds target periodic distributions, often with a stated preferred return. Terms vary, and there are no guarantees. Read the PPM.

- Tax Efficiency: Apartments depreciate on a 27.5-year MACRS schedule; cost-segregation studies may accelerate deductions. Passive allocations generally flow through a K-1 and are subject to the passive activity rules.

- Inflation Hedge: Leases reset, operating expenses can be managed, and well-run multifamily assets tend to absorb some inflation over time. Those factors make it a great hedge against inflation.

- Diversification: Spread exposure across multiple units, markets, and fund types.

Macroeconomic Trends Shaping Multifamily Real Estate Funds in 2025 and 2026

When peeling back the layers, the story of multifamily demand in 2025 and 2026 isn’t only about why people rent. It’s also about how much new housing supply is actually coming online. In 2025, we’re on the edge of a supply and demand imbalance that could define returns for years to come.

Demographics: A Deeper Renter Pool

Millennials are still renting longer as affordability keeps homeownership out of reach. Gen Z is also entering prime household-formation years, and seniors are downsizing into rentals that better fit their lifestyles. Together, these cohorts create a wide, steady renter base for investors to tap into.

That keeps household formation flowing even in markets where ownership costs may soften.

Migration Patterns: Normalization with a Midwest and Sunbelt Tilt

Remote and hybrid work continues to influence household choices. While the pandemic-era migration surge and the proclivity of remote work have cooled, the Midwest and Sunbelt still benefit from relative affordability and job growth. Secondary and tertiary markets with durable employment anchors (not just “zoom towns”) are seeing sustained leasing demand.

Housing Affordability: Sticky Rental Demand

For many Americans, the affordability gap between renting and owning remains wide. Mortgage rates may stabilize if interest rates are lowered, but entry-level home supply is scarce, and prices remain elevated. Lowering rates could result in a surge in demand, increasing the asking price for existing homes.

These dynamics will likely keep many households renting longer, translating into consistent demand for multifamily units, even when rents rise modestly.

Supply on the Brink: From Oversupply to Shortfall

New construction for housing peaked in 2024, but has since fallen sharply. Deliveries are set to taper in 2025 and drop even further in 2026, creating a supply contraction just as renter demand steadily increases.

- Markets with heavy 2024 completions (e.g., Sunbelt metros) are still digesting excess inventory. Absorption is slower, concentrations are higger, and rent growth is muted.

- Markets with limited pipelines (e.g., Midwest and select coastal markets) are already seeing healthier occupancy and firmer rent growth because there are few new products to compete with existing assets.

Funds positioned in supply-disciplined markets may see stronger rent and NOI growth, while funds concentrated in oversupplied markets could lag behind in 2026.

Interest Rate Environment: From Headwind to Stability?

The rate shock of 2022-2023 has given way to a steadier footing. Stabilizing interest rates makes underwriting cleaner and helps restore transaction volume. For funds, this environment supports more rational pricing and allows institutional investments to sharpen focus on multifamily’s risk-adjusted stability relative to many other asset classes.

The Core Takeaway

Demand is still climbing while supply appears to be bending down. That mismatch sets the stage for higher occupancy and rent growth in balanced markets (and for headaches in overbuilty ones).

Multifamily real estate funds that choose markets and vintages carefully will be well-positioned to capture that divergence.

BAM Capital’s Approach

At BAM Capital, we focus on providing accredited investors with access to multifamily real estate funds and deals that seek to create durable results. Here’s how we accomplish that.

- Investor-centric focus: We provide clear reporting, timely K-1s, transparent insight into how your money works, and distribution policies that reflect realistic property-level cash flow instead of aggressive projections.

- Midwest market edge: We target regions that have historically proven to provide and are forecasted to continue providing stable employment bases, balanced supply pipelines, and lower volatility than boom-and-bust markets.

- Conservative underwriting and due diligence: Our investment strategy approach emphasizes moderate leverage, stress-tested exit assumptions, and ample reserves to withstand unexpected market conditions.

- Vertical integration: We handle everything in-house, from acquisition to exit. This allows us to control every aspect of performance drivers and operational execution.

- Institutional-quality assets: We offer multi-asset funds and select single-asset deals where construction is warranted.

- History of exits and realized returns: We have successfully executed full-cycle multifamily investments across market cycles, delivering gross realized equity multiples and gross IRRs in line with or exceeding our conservative underwriting assumptions. All while maintaining a strong record of preferred distribution performance. These gross returns, along with the corresponding net returns and full portfolio performance, are detailed in the track record snapshot below.

Track Record Snapshot

*Carousel of your track record from other pages goes here*

Looking Ahead with BAM Capital

Multifamily real estate funds give accredited investors a practical way to access large-scale housing assets without taking on the day-to-day ownership work. At BAM Capital, we stick to Midwest markets, keep leverage conservative, and run operations in-house so we can control the details that matter most.

If you’re considering how multifamily might fit into your long-term plan, take a closer look at our approach and our track record.