What is real estate syndication? It’s when a group of investors pool their money to buy income-producing property—usually something big like an apartment complex—with a sponsor who handles the heavy lifting.

The sponsor, also called the general partner (GP), is responsible for finding the deal, securing financing, managing the property, and eventually selling it. Investors like you come in as limited partners (LPs), contributing capital without having to deal with the day-to-day management.

For accredited investors, real estate syndications offer a way to earn passive income, diversify portfolios, and access commercial-grade real estate that would normally be out of reach. In this guide, we’ll walk you through how it all works, what to expect, and what to look for in a quality sponsor.

Topics covered:

- How Real Estate Syndication Works

- Key Terms

- Internal Structure of a Syndication

- Types of Syndications (With Comparisons)

- Benefits of Real Estate Syndication for Investors

- Risk to Consider and How to Evaluate Them

- Real Estate Syndications vs Other Real Estate Investment Options

- What to Look for in a Syndication Sponsor

- Who Is Real Estate Syndication Right For?

- Finding the Right Partner for Your Portfolio

How Real Estate Syndication Works

When people ask “What is a real estate syndication?”, this is one of the main things they’re asking. Syndications aren’t just a buy, hold, and hope investment vehicle. They are well-structured investment options that involve planning, partnership, incentives, and capital deployment.

Everyone involved has a role, and when it’s done right, it can be great for investors’ portfolios.

Before we dive in, here are some important key terms that will help you understand the rest of the guide:

Key Terms You’ll Hear Often

- Limited Partner: The passive investor providing a portion of the capital.

- General Partner: The active sponsor managing the deal.

- Preferred Return: A fixed return (e.g., 8%) that LPs receive before the GP shares in profits.

- Promote: The GP’s share of profits after LPs have received their preferred return.

- Equity Waterfall: This structure governs how profits are distributed. Capital is usually returned to LPs first, then the preferred return, and finally, profits are split. (e.g., 60/40 LP/GP)

- Hold Period: The projected timeframe (typically 2-10 years) that assets are held in a fund.

- Internal Rate of Return (IRR): A metric that calculates the overall return, factoring in both cash flow and the timing of those returns. IRR targets can vary anywhere from 6%-25% based on the strategy used.

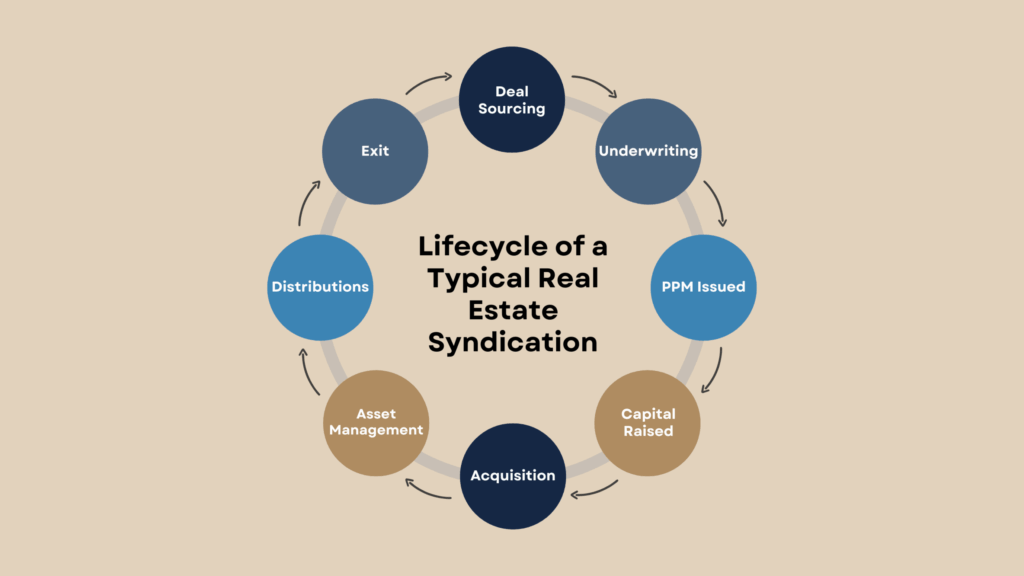

A Closer Look at The Internal Structure of a Syndication

Deal Sourcing and Underwriting by the GP

The syndication process typically kicks off with the GP hunting down a property (or a few) that line up with the fund’s overall investment strategy. That means digging into the market, finding deals that aren’t broadly listed, and running the numbers to see if it all pencils out.

A good GP will underwrite the deal by taking a hard look at:

- Rent growth potential

- Occupancy trends

- Renovation scope and budget

- Projected net operating income (NOI)

- Expected exit value based on market cap rates

The end goal? To put forward a deal that delivers returns and fits squarely into the fund’s focus (e.g., value-add multifamily in dependable Midwest markets).

Capital Pooling from LPs

Once the deal’s under contract, the GP brings it to accredited investors by way of a Private Placement Memorandum—what we call a PPM. At that point, LPs can commit capital, typically starting anywhere from $25K-$250K+. That capital gets pooled to cover the equity side of the deal and formalizes each investor’s stake in the project.

Acquisition and Asset Management

After closing, the GP oversees renovations (if it’s a value-add deal), day-to-day operations, and property management. LPs receive regular updates and financial reports while enjoying passive income distributions as outlined in the PPM.

Some GPs use a vertically integrated structure, meaning they handle everything in-house—from acquisition through management and final sale. Others choose to outsource certain functions, like property management or construction, which can work just fine but may introduce more variables regarding quality control and accountability.

Profit Distribution and Exit Strategy

Profits are shared according to a predetermined structure, starting with a preferred return to LPs and followed by a split of additional profits (the promote) between LPs and the GP. After several years, known as the hold period, the property is sold or refinanced to return investor capital and additional gains.

While real estate syndications provide many similar benefits, no two deals are the same. However, most syndications follow a general lifecycle like the one shown below.

⚠️ Note: The flow shown here is a typical example. The exact process and lifecycle of a syndication may and likely will vary based on the fund’s structure and the sponsor’s return structure and investment strategy.

Types of Real Estate Syndications

Syndications can be structured in various ways, each with its own pros and tradeoffs in terms of risk, transparency, etc. Here’s a quick breakdown of each.

Single-Asset vs. Multi-Asset Syndications

Single-Asset Syndication

This structure focuses on one specific property. For instance, a 250-unit apartment complex. It’s more straightforward to underwrite and easier for LPs to evaluate. But with all capital tied to a single asset, you’re exposed to concentrated risk. If that one deal underperforms, there’s no alternative.

Benefits  |

Potential Concerns  |

|---|---|

| Easier for GPs to underwrite and LPs to evaluate. | All of the LPs’ eggs are in one basket, creating higher risk exposure. |

| Greater visibility since everything is tied to a single deal. | No cushion if the deal underperforms. |

| Shorter deployment timeline. | Fully exposed to local market shifts. |

Multi-Asset Syndication

Conversely, in this model, the GP uses the pooled capital to acquire a portfolio of properties, either upfront or over the course of the syndication. This creates built-in diversification, smoothing out risk across multiple locations or asset types. However, these may be more complex to evaluate and have a longer hold period.

| Benefits |

Potential Concerns |

|---|---|

| Built-in diversification reduces overall risk. | More complex for GPs to underwrite and LPs to evaluate. |

| Smoother cash flow across the portfolio. | Longer timeline to deploy capital. |

| One investment gives you exposure to several properties. | Capital may be deployed more gradually. |

Blind Pool vs. Specified Offerings

Blind Pool

LPs commit capital before the specific properties are identified, based on a clear understanding of the asset types, investment strategy, and the GP’s proven track record. This structure provides the GP with flexibility to act on high-quality opportunities as they arise, while requiring confidence in the sponsor’s experience and disciplined approach.

| Benefits |

Potential Concerns |

|---|---|

| Gives the GP flexibility to act fast on deals. | LPs invest without knowing the exact properties. |

| Can access stronger pipelines if GP has capital ready to deploy. | Higher reliance on the GP’s track record and discipline. |

| Useful for long-term strategy execution. | May not match every LP’s preference. |

Specified Offering

In a specified deal, the property(s) have already been identified, underwritten, and often placed under contract. LPs can analyze it before committing capital, which increases the level of transparency.

| Benefits |

Potential Concerns |

|---|---|

| Full property details are available at commitment. | GP has less flexibility. |

| Easier to evaluate the opportunity upfront. | May require faster decision-making by the investor. |

| More confidence in what capital is backing. | Limited to one known asset at a time. |

Benefits of Real Estate Syndication for Investors

While each kind of syndication comes with its own benefits and potential concerns, there are general benefits that LPs can expect to enjoy across all forms of syndications. These include:

- Passive Income: Investors enjoy cash flow from a truly passive investment vehicle, thanks to sponsors managing the syndication and funds. That means no tenant calls, dealing with plumbing issues, or worrying about repairing expensive AC units.

- Access to Institutional-Quality Assets: Individual investors rarely can afford to purchase institutional-quality real estate like apartment complexes or condominiums. Syndications allow investors to access such assets at a fraction of the cost.

- Tax Advantages: LPs may benefit from unique tax advantages such as depreciation, cost segregation, and potentially 1031 exchange eligibility. (Consult your tax advisor for

- individual guidance.)

- Depreciation deductions can offset income.

- Cost segregation accelerates depreciation.

- 1031 exchanges allow the deferral of capital gains taxes in some scenarios.

- Diversification: Syndications will often spread risk across markets, asset types, and strategies.

- Markets (e.g., Midwest, Sunbelt, secondary metros).

- Asset types (e.g., value-add multifamily, stablized core-plus).

- Strategies (core, core-plus, value-add, opportunistic, income-focused, growth-focused).

- Professional Management and Guidance: Experienced GPs bring proven acquisition and operational expertise.

Risk to Consider and How to Evaluate Them

Like any real estate investment, syndications are not risk-free. Key considerations include.

Market Risk

Real estate values can fluctuate due to many factors.

What to Look For

- GP’s Market Selection: Are they investing in strong job-growth metros with diverse economies and strong rental demand?

- Conservative Rent Growth Assumptions: Are they assuming 3-5% growth or 10%? Unrealistic growth expectations could be a red flag.

- Vacancy buffers: A good underwriting model bakes in some vacancy or bad debt cushion, just in case.

Sponsor Risk

This is possibly the biggest one–and often the most overlooked. Even a great property(s) can underperform if the sponsor overleverages, mismanages the asset, or isn’t transparent with investors

What to Look For

- Track Record: Has the GP done syndications before? Have past deals hit their projected IRRs and preferred returns? While past performance is not indicative of future

- results, it can be helpful information.

- Fee Structure: Are the fees reasonable? Are returns net of fees? Or are they nickel-and-diming the deal before investors even see a return?

- Transparency: Do they communicate clearly and consistently? Investors should expect quarterly reports, financial statements, and real-time updates on their investments.

- Skin in the Game: Is the GP also investing its own capital? If not, how are they held accountable for performance?

- Exit Discipline: Does the GP sell when the time is right?

Illiquidity

Syndications are not liquid like stocks or public REITs. Once investors are in, their money is typically tied up for the holding period.

What to Consider

- Can the investor afford to lock up that capital for several years?

- Is there an option noted in the PPM for an early exit or liquidity in extreme cases (some sponsors may offer internal buyouts, but most do not)?

Underperformance

Not every deal hits the target IRR. Rents may not grow as quickly as expected, expenses may rise, or renovation plans may exceed budget.

What to Watch For

- Aggressive pro formas: If the numbers look too good to be true, they probably are.

- Lack of stress testing: Has the sponsor shown what happens if rents stay flat or vacancy rises?

- Value-add plans: Are renovations realistic and costed properly?

Real Estate Syndications vs Other Real Estate Investment Options

When weighing real estate investment options, it helps to see how the benefits and potential concerns of syndications stack up against other common real estate vehicles.

Below is a chart that broadly compares the most popular real estate investment options.

| Feature | Syndication | Direct Ownership | REIT (Public) |

|---|---|---|---|

| Ownership | Indirect; sponsor owns and manages property. | 100% ownership of a single property | Shares in a company that owns real estate |

| Control | None; LPs are passive investors | Full control over decisions | None |

| Minimum Investment | Higher; $25K-$250K+ | Lower; may only require down payment on property with mortgage | Low; as little as $100 |

| Liquidity | Illiquid; generally a 2-10 year holding period | Illiquid; until investor sells | Highly liquid; can sell on stock market |

| Cash Flow Potential | High; distributions can be made quarterly, annually, and at end of fund | High; self-managed property with rental income | Moderate; often lower yields |

| Tax Benefits | Depreciation, cost seg, potential 1031 exchange eligibility | Same as syndication; if structured properly | Limited; often taxed as dividends |

| Investor Time Commitment | Extremely Low; fully passive | Very high; active management required unless using a property management company (which cuts into profits) | Low; passive aside from worrying about share prices |

| Return Potential | Strong; 8-20% target IRR for many syndications | Depends highly on property and management skill | Lower; limited correlation to equities |

What to Look for in a Syndication Sponsor

A practical checklist to help readers vet potential GPs:

- GP Co-Investments and Alignment of Interests: If the sponsor doesn’t have skin in the game, it could be a red flag. Investors should look for a GP that is putting its own money into the deal and sharing risk–not just collecting fees on the front end.

- Sponsor Track Record and Transparency: Investors should prioritize a sponsor that has been through a complete market cycle or at least has a track record of getting deals across the finish line. Fancy pitch decks mean little if they can’t execute.

- Fair Fee Structure: Fees aren’t bad. They’re an inherent part of any syndication to help ensure its success. But they should be reasonable and tied to real value creation–not padded in every direction.

- Promote Structure Tied to Performance: The promote is the GP’s share of the profits, and that is fair if it comes after investors are made whole. However, some sponsors may try to take a cut before hitting even basic benchmarks.

- Do You Understand Their Strategy–Does it Fit Your Goals?: Even the best operator can run a deal that isn’t a good fit for certain investors. If an investor doesn’t understand the business plan or if it simply doesn’t line up with their goals, risk tolerance, or timeline, it might not matter how strong the returns look on paper.

Who Is Real Estate Syndication Right For?

While real estate syndications aren’t for everyone, they can be a great way for the right investor to put capital to work without worrying about the hassle and headaches of managing real estate themselves.

It may be worth a closer look if any of these sound like they fit.

Accredited Investors

Private placements like these often aren’t available to just anyone.

If you qualify as an accredited investor–net worth over $1 million (not counting primary residence) or you have a high enough income–$200K alone or $300K with spouse–you meet the SEC definition of an accredited investor.

These are typically the only individuals who are allowed to invest in real estate syndications. So, naturally, this is the first place to start.

Passive Investors Who Want to Get Off the Roller Coaster

If you’re an investor who is tired of watching the stock market bounce around and would prefer access to steady cash flow that isn’t as tied to headlines or tech earnings, syndications can offer a more predictable income stream.

They tend to perform well in both bull and bear markets and are considered hedges against inflation, especially when structured with good, conservative underwriting.

Ex-Landlords Who Are Done with 2 A.M. Calls

If you’ve owned rental properties before, but you’re ready to stop being the one ultimately responsible for fixing air conditioners and toilets and negotiating with contractors, Syndications let you stay in real estate, collect income, and build equity without the day-to-day annoyances.

High-Income Professionals Looking for Tax Relief

If you’re a doctor, executive, lawyer, or other high-income earner with a sizable W2 income, you know that the tax bill every April can sting. Syndications can help. You may get pass-through benefits like depreciation through cost segregation that could potentially lower your tax burden.

Investors Focused on Diversification and Scale

Let’s say you’re already invested in stocks and mutual funds and want to spread your exposure. Or maybe you don’t want to sink all your capital into one local rental.

Real estate syndications can allow you to split an allocation of capital, say $200K, across multiple markets, asset types, and strategies (depending on the fund).

Ultimately, if you’re an accredited investor who likes the idea of owning a piece of high-quality real estate, wants strong cash flow, and doesn’t have the time (or patience) to manage it yourself, syndication could be a great fit.

Just make sure the strategy makes sense and you conduct due diligence on the sponsor behind the deal.

Why BAM Capital Could Be the Right Partner for Your Portfolio

If you came here asking, “What is real estate syndication?”—we hope this guide gave you a clear, practical answer. More importantly, we hope it helped you see whether syndication aligns with your financial goals.

At BAM Capital, real estate syndication is at the core of building and managing our funds. We take the model seriously, not just because of its potential return but also because of how it can be structured to benefit investors.

Here’s how we do that:

- We focus on multifamily investing in secondary Midwest markets with strong job growth, population stability, and limited new supply—places where fundamentals still make sense.

- We underwrite conservatively, bake in vacancy and expense buffers, and avoid relying on aggressive rent growth to hit our targets.

- We co-invest alongside our Limited Partners in every deal, so your money is right there next to ours.

- We prioritize transparency, with quarterly distributions, detailed investor reports, and a secure portal so you always know where your investment stands.

Our leadership team brings over 215 years of combined real estate experience, and we’ve earned a strong reputation for our commitment to executing our strategy and maintaining transparency.

If you’re an accredited investor looking for a trusted partner in passive real estate, we’d love to earn your confidence. Let’s talk about whether BAM Capital is the right fit for your portfolio.

Ready to see if we’re the right fit for your portfolio? Schedule a call today to learn how BAM Capital can help you build long-term wealth through our real estate syndication returns.

Disclaimer: This article is for informational purposes only and is not financial, legal, or investment advice, nor an offer or solicitation to buy or sell securities. BAM Capital and its representatives are not fiduciaries. Investment opportunities offered by Bam Capital are made pursuant to Rule 506(c) of Regulation D and are available exclusively to accredited investors, as defined by the Securities and Exchange Commission (SEC) and, if applicable, qualified purchasers. Verification of accredited investor status is required before participation in any investment.

Any financial terms, projections, or forward-looking statements contained herein are hypothetical in nature and should not be interpreted as guarantees of future performance or safety. Such statements are based on current expectations, estimates, and assumptions, which are inherently subject to uncertainties and contingencies, many of which are beyond Bam Capital’s control. Such statements reflect Bam Capital’s opinion and are subject to market fluctuations, economic conditions, and investment risks. Actual results could differ materially from those projected or implied in any forward-looking statements.

Investing in private real estate securities involves significant risks, including but not limited to illiquidity, economic downturns, and potential loss of invested funds. Past performance does not guarantee future results. Prospective investors are strongly encouraged to conduct independent due diligence and consult with legal, tax, and financial advisors before making any investment decisions.

© 2025 Bam Capital. All rights reserved.